time to read: 29min

download the article (PDF 347kb)

Executive Summary

The contemporary surge in artificial intelligence (AI) investment across the Western world is widely portrayed as the emergence of a general-purpose technology capable of restoring productivity growth and inaugurating a new regime of accumulation (McGeever 2025). Yet the scale, concentration, and urgency of this investment wave, unfolding alongside weak generalized productivity gains and uneven enterprise diffusion, point to a more structural crisis dynamic (Brynjolfsson, Rock and Syverson 2017). Under conditions of stagnating productive returns, AI has become a privileged outlet for valorizing surplus capital (Carlos Bresser-Pereira 2024; Desai 2025). In the oft-neglected sphere of Marxian economics, the present conjuncture reflects a situation in which “the real barrier of capitalist production is capital itself” (Marx 1894, pt. III, ch. 15), such that capital unable to secure adequate returns in production multiplies “accumulated claim[s], [and] legal title[s], to future production” (Marx 1991, ch. 29, n.p.). The AI boom thus operates less as a durable resolution of stagnation than as a spatio-temporal displacement[iii] of overaccumulation[iv] pressures through enclave concentration, credit expansion, and promissory valuation.

This displacement has direct macro-financial and strategic consequences. AI-related capital expenditures and equity gains are increasingly concentrated in a narrow cluster of firms and upstream infrastructures, while measured productivity effects lag behind the scale of committed capital. In a financial system organized around credit-based temporal deferral and expectations of liquidity support, such concentration heightens systemic vulnerability. A sharp repricing would transmit beyond technology firms into pension portfolios, labour markets, fiscal balances, and state capacity (Cochrane 2005). Crisis adjustment historically destroys livelihoods more readily than capital, consolidating market power among surviving firms and deepening dependence on public guarantees (Harvey 2018).

Federal policy should therefore treat AI not only as an innovation agenda but as a macro-financial and strategic-industrial exposure. Governments should require disclosure and stress testing of AI-linked concentrations across pensions and non-bank finance; condition monetary and industrial support so that cheap credit does not inflate the “money [supply] that is thrown into circulation as capital without any material basis in commodities or productive activity” (Harvey 2018, 95); and redirect surplus investment toward socially necessary and security-relevant infrastructures such as energy resilience, housing, and publicly governed technology. The objective is not to suppress technological development, but to prevent repeated speculative cycles from amplifying systemic risk while leaving underlying stagnation unresolved.

The AI Investment Surge in Context: Productivity Promises and Structural Stagnation

The contemporary surge in private artificial intelligence (AI) investment is widely narrated, in neoclassical economics and policy discourse, as a technological revolution: a general-purpose technology (GPT) poised to inaugurate a new regime of productivity and, by extension, accumulation (McGeever 2025). Across venture capital, corporate strategy, and state industrial policy, AI is positioned as the spearhead of a renewed growth trajectory capable of overcoming the secular stagnation[v] that has marked advanced capitalist economies since the late twentieth century (Andreessen 2023). Yet the very insistence with which this promise is repeated, despite limited realized productivity effects, indicates that something more than a linear technological transition is at stake (Brynjolfsson, Rock and Syverson 2017).

Accordingly, this report argues that Silicon Valley’s AI boom should not be misinterpreted as a general-purpose technological breakthrough inaugurating a “Fourth Industrial Revolution” (Crafts 2021, 522; Schwab 2017). Rather, it is more coherently interpreted as a symptom of overaccumulated capital’s growing difficulty in securing profitable outlets within productive accumulation, and thus as a speculative displacement of stagnation rather than its resolution.

The present conjuncture closely parallels earlier episodes of speculative expansion, most notably the dot-com boom of the late 1990s (Youvan 2025), but unfolds under conditions in which the spatial-fixes that once absorbed surplus capital, that is, the geographical displacement of overaccumulated capital into new markets, infrastructures, and territorial expansions (Harvey 2001), are increasingly constrained by intensifying international protectionism and tariff regimes (Goodell Ugalde 2025a). Accordingly, AI-centred investment, even relative to the dot-com bubble, disproportionately amplifies the market’s promissory expansion of “accumulated claim[s], [and] legal title[s], to future production” (Marx 1991, ch. 29, n.p.) without generating corresponding increases in current output or surplus-value production.

The resulting paradox is therefore familiar: unprecedented volumes of capital are mobilized in the name of productivity, while measurable productivity growth remains stubbornly weak. This dynamic is best interpreted as a crisis-displacement mechanism in which, as Harvey observes, “capital never solves its crisis tendencies, it merely moves them around” (Harvey 2010, 116). In the present conjuncture, this displacement is mediated through technological exuberance and what Desai describes as “phantastical goals” (2025, 7), narratives that sustain large-scale investment by projecting transformative future productivity gains. Such expectations defer rather than resolve the underlying contradictions of accumulation, while simultaneously generating significant systemic economic risk.

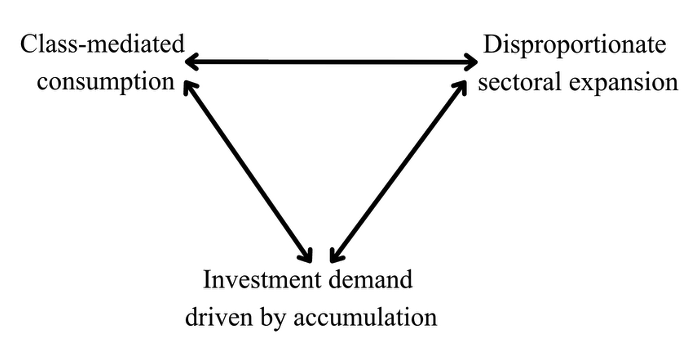

On this reading, the Western hemisphere’s capital-intensive AI investment model conforms closely to Paul Baran and Paul Sweezy’s account of monopoly capitalism and reproduces its characteristic structural vulnerabilities and economic security risks. Silicon Valley’s prevailing AI investment regime aligns with their framework in three interlocking respects whose combined effects “far exceeds the sum of each part” (Whiting and Park 2023, n.p.): (i) class-mediated consumption, including elite and institutionally anchored demand; (ii) investment demand driven by the imperatives of accumulation rather than realized productive necessity; and (iii) disproportionate sectoral expansion that concentrates accumulation within a narrow economic enclave (Baran and Sweezy 1966) (fig. 1).

|

|

Figure 1. The dialectical interaction between three counter-tendencies to the tendency of the rate of profit to fall, interpreted through the monopoly-capital framework developed by Paul Baran and Paul Sweezy (1966). |

From Realization to Financial Deferral: How Surplus Capital Finds Technological Outlets

Neo-Marxist political economy has long examined how counter-tendencies to declining profitability take determinate historical form, first through imperial expansion and later through the deepening of credit and finance. Rosa Luxemburg’s distinctive intervention was to interpret economic imperialism not as a contingent policy choice but as a structural outlet rooted in the realization problem under expanded reproduction. In The Accumulation of Capital (1963), she argues that surplus value cannot be fully realized within a “pure” or closed market totality because internal demand is structurally bounded: workers’ consumption is limited by wages, while capitalists’ consumption and investment are constrained by the requirements of accumulation itself. Hence, the “realization of the surplus value … requires … that there should be strata of buyers outside capitalist society,” since surplus value “cannot be realized by sale either to workers or capitalists,” but only through sale to “social organizations or strata whose own mode of production is not capitalist” (351–52).

In more straightforward economic terms, the dynamic can be understood as a tension between expanding productive capacity and the limits of effective demand: Firms seek to increase profitability by improving efficiency, often through automation, technological investment, or reductions in labour costs. While such strategies may raise productivity at the level of individual firms, they also suppress aggregate purchasing power if wage growth slows or employment opportunities decline. Following, because households remain the primary consumers in most advanced economies (World Bank 2026), weaker wage growth can translate into weaker demand across the wider economy. When production capacity expands faster than effective demand, firms may find themselves with more goods, services, and investment capacity than markets can profitably absorb. The result is a situation in which capital and productive capacity accumulate more rapidly than the economy’s ability to sustain profitable investment, generating swaths of “over-accumulated capital” that “can’t be laid aside as ‘unused’” (Harvey 2026; Clarke 1990). For Luxemburg, the historical resolution to this problem lay in the outward expansion of capitalist markets: by incorporating new territories, populations, and social relations into circuits of exchange, firms could access new markets capable of absorbing surplus output and thereby temporarily restore the conditions for continued accumulation, what may later be dubbed “the “spatial fix” (in the sense of geographical expansion to resolve problems of overaccumulation)” (Harvey 2001, 28).

Economist Paul Sweezy reformulates this diagnosis by rejecting Luxemburg’s claim that realization is logically impossible within a closed market sphere. Rather than positing a formal contradiction, he treats realization as a chronic instability internal to capitalist reproduction. In The Theory of Capitalist Development, he takes up Luxemburg’s decisive question, “where is the demand for the [over] accumulated surplus value?” (1942, 202), yet rejects the view that its resolution must necessarily depend on spatial displacement through market expansion, even if historically it has often taken precisely that form, particularly through imperial and neo-imperial expansion (Bieler et al. 2016).

Nevertheless, Sweezy (1942) instead foregrounds a provisional resolution through temporal displacement via credit and finance, a dynamic later captured as the circulation of “money that is thrown into circulation as capital without any material basis in commodities or productive activity” (Harvey 2018, 95). On this view, even a relatively closed market can temporarily absorb overaccumulated surpluses through historically specific institutional arrangements such as employment growth, the expansion of variable capital,[vi] credit creation, state expenditure, or the opening of new markets. Such mechanisms do not restore equilibrium, however. Rather, they defer the underlying contradiction by sustaining demand through increasingly unstable financial and institutional supports.

Against Luxemburg’s conclusion that internal accumulation ultimately becomes “a merry-go-round which revolves around itself in empty air,” Sweezy argues that realization does occur, but only as an unstable achievement that intensifies rather than resolves capitalism’s crisis tendencies (Sweezy 1942, 203). In practice, this dynamic frequently appears through policy and financial mechanisms that expand domestic purchasing power without corresponding increases in productive capacity. Governments may, for example, lower interest rates to stimulate consumption and investment, encouraging households and firms “to take on more debt than they should” (Tranjan 2023, 8). Alternatively, financial markets may channel surplus capital into rapidly expanding asset classes whose valuations are sustained less by realized profitability than by the continued expansion of credit. Such assets simultaneously function as sinks for surplus investment and as speculative vehicles whose prices are themselves inflated by the very credit expansion that makes them possible.

Financial expansion therefore displaces rather than resolves the contradictions of overaccumulation within the economy. What Arrighi describes as “temporal deferral” functions as a provisional “fix” for crises that arise when capital accumulates beyond what can be profitably reinvested in commodity production and exchange (Arrighi 2006, 202).

In later work, Sweezy, together with Paul Baran, extended this analysis by examining how advanced capitalist economies absorb persistent surpluses under conditions of monopoly capitalism. In Monopoly Capital (1966), they identify three principal channels through which surplus absorption is sustained. Reformulated here, these mechanisms can be understood as: (i) class-mediated consumption, in which surplus is absorbed through socially stratified expenditure patterns; (ii) investment demand driven by the imperatives of accumulation itself rather than by demonstrable productive necessity; and (iii) disproportionate sectoral expansion, whereby accumulation becomes concentrated within a narrow and increasingly insulated enclave of the broader economy.

Each is paradigmatic of the contemporary AI investment cycle. Together they generate a crisis pathway that is not accidental but structurally predictable: demand is sustained through socially selective expenditures and reputational adoption, capital formation becomes increasingly self-referential and credit dependent, and growth is concentrated in an enclave whose valuations rest on promissory horizons rather than realized surplus value and production. When those horizons contract, in what neoclassical economics would describe as a “bubble bursting,” (Caballero 2016) the adjustment assumes a familiar pattern: rapid devaluation and credit contraction, followed by layoffs, pension and portfolio losses, fiscal strain, and intensified consolidation as surviving firms absorb market share, deepen oligopolistic control, and heighten systemic economic fragility.

Demand Engineering and Institutional Adoption: The Political Economy of AI Uptake

Sweezy and Baran’s first surplus absorption mechanism, class-mediated consumption, is often reduced to elite luxury spending (Feldman, and Bellamy Foster 2015). In Monopoly Capital (1966), however, the concept is structural. It refers to the expansion of surplus-absorbing expenditures that are socially selective, institutionally organized, and only weakly anchored to the “real economy”, understood here as economic activity tied directly to the production and consumption of goods and services rather than to financial market activity (Cochrane 2005).

The point is not simply that affluent strata consume more, but that accumulation comes to rely on a “qualitatively different thing …. differing qualitatively from the preceding, the former state” (Bukharin, 2013, 79–80). Under monopoly capitalism, expenditure streams increasingly serve the systemic function of realizing surplus value under conditions where both productive investment and mass consumption are constrained. As Baran and Sweezy emphasize, the “normal modes of surplus utilisation” become persistently insufficient, such that “the question of other modes of surplus utilisation assumes crucial importance” (Baran and Sweezy, 1966, 13).

Their central name for this manufactured demand is the “sales effort,” an enlarged apparatus of market making and demand engineering that fabricates effective demand when markets do not expand organically. They describe it as “identical with Marx’s expenses of circulation,” but insist that under monopoly capital it plays a role “both quantitatively and qualitatively, beyond anything Marx ever dreamed of” (Baran and Sweezy, 1966, 114). It is therefore not a marginal supplement to accumulation but a countervailing mechanism that “turns out to be a powerful antidote to monopoly capitalism’s tendency to sink in a state of chronic depression,” precisely because it “absorbs, directly and indirectly, a large amount of surplus which otherwise would not have been produced” (Baran and Sweezy, 1966, 131, 125). Its expansion signals a shift in competitive strategy away from productivity and price and toward the organized production of perception, expectation, and dependence, a dynamic inseparable from capitalism’s “colossal capacity to generate private and public waste” (Baran and Sweezy, 1966, 3).

The contemporary AI boom fits this logic. Much of what is described as AI adoption does not correspond to generalized diffusion of demonstrably productivity enhancing techniques, rather what Desai calls a “cultish hype about technology driving vast over-investment” (2025, 6). Increasingly, adoption takes the form of prestige expenditure aimed at signalling technological relevance and organizational modernity. Firms, universities, hospitals, and state agencies adopt AI not primarily because it reliably raises output, but through competitive and reputational pressure, including “bandwagon effects, where firms rush to adopt AI-driven marketing solutions” (Ozturkcan and Bozdağ 2025, 700). AI thus functions as luxury infrastructure, a high status organizational input whose legitimacy effect often exceeds its realized contribution to surplus value production.

This sales effort dynamic now extends well beyond advertising into organization wide “digital transformation” programs. As Sciuk et al. describe, these are “holistic and profound organizational changes” that mobilize heavy spending on consultants and integration vendors, proliferating pilot projects, compliance and governance regimes, procurement procedures, “roadmaps,” and internal restructurings (Sciuk, Engert, Gierlich-Joas and Hess, 2025). Because digital transformation is a “moving target,” firms are drawn into repeated cycles of “experimenting and piloting” that frequently fail to scale. Indeed, “86% of digital transformation projects fall notably short of their objectives” (6–9). Yet these expenditures remain economically functional. They generate contracts, billable hours, software revenues, and recurring service streams, while absorbing surplus in forms that do not require commensurate increases in labour productivity. In Baran and Sweezy’s terms, they are organized modes of surplus utilisation that sustain demand and activity when accumulation cannot proceed smoothly through productive investment alone.

State-Backed Accumulation: Guarantees, Subsidies, and Strategic Industrial Policy

Baran and Sweezy’s second surplus absorption mechanism, investment demand generated by accumulation itself, names a configuration in which investment ceases to function primarily as a response to expanding markets or realized productivity gains and instead becomes structurally self-referential. Under monopoly capitalism the decisive contradiction is less the production of surplus than its absorption. Economic surplus, defined as “the difference between what a society produces and the costs of producing it,” (Baran and Sweezy 1966, 9) exhibits a secular tendency to rise as productivity advances under conditions of administered prices and restricted output (Dawson and Foster, 1992). Crisis emerges when accumulation cannot proceed, since the “cessation of further accumulation constitutes the crisis situation, which Marx characterized as one of overaccumulation” (Mattick 1974, n.p.). In this context financialization marks a “shift in gravity of economic activity from production … to finance” (Bellamy Foster 2007, n.p.), functioning as a means of “kicking the can down the road” (Cutrone 2017–18, n.p.) by deferring the reckoning that stagnation otherwise imposes.

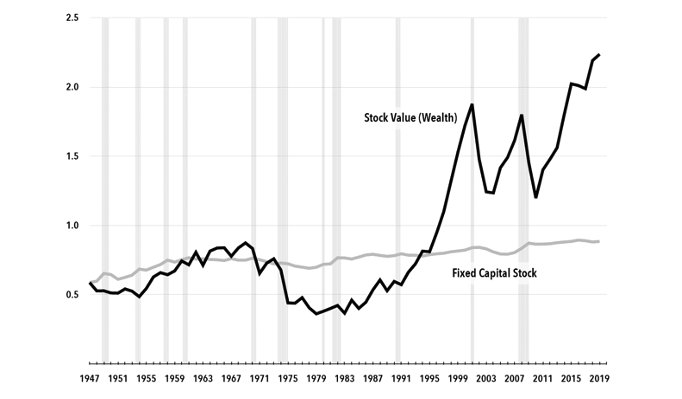

John Bellmay Foster stresses, however, that this process “falls short of a whole new stage of capitalism, since the basic problem of accumulation within production remains the same” (2007, n.p.). Its importance is therefore not merely rhetorical inflation around technology or finance, but the way such narratives mediate a regime in which capital is “trapped in a seemingly endless cycle of stagnation and financial explosion” (2007, n.p.). As overaccumulated surplus grows, reinvestment becomes a compulsion oriented toward preserving value through motion rather than expanding socially necessary production. Investment is progressively decoupled from demonstrable productive need and organized around anticipatory expectations, speculative narratives, and institutional supports that sustain accumulation without corresponding increases in surplus value production. The resulting claims on future productivity appear “suspended in thin idealist air” (Ashley 1984, 247). Investment demand thus becomes referential to accumulation itself, functioning as a temporary absorber of surplus under chronic stagnation rather than as a driver of material productivity (Fig 2).

|

|

Figure 2. The graph shows that since the mid-20th century (especially after the 1990s) stock market wealth has grown dramatically and increasingly diverged from the much more gradual rise in fixed capital stock, indicating a widening gap between financial asset values and underlying productive investment (Clark, Bellamy Foster, and Jonna 2021). |

Once again, the contemporary AI boom exemplifies this dynamic. As Desai puts it, “a senile capitalism is unable to muster enthusiasm about any project unless it combines vast amounts of capital, expectations for huge returns and huge state guarantees and subsidies” (2025, 14). AI emerges less as a response to demonstrated productive demand than as a demand generating investment object, able to mobilize capital precisely because it promises transformative futures while deferring profitability tests. This is the terrain Marxist economics and the monopoly capital tradition describe as accumulation increasingly mediated by fictitious claims, including “fictitious capital, detached from tangible assets, and thus detached from any socially necessary labour time” (Goodell Ugalde 2016, 288). Accumulation becomes “twofold,” combining “the ownership of real assets and also the holding of paper claims to those real assets” (Bellamy Foster 2007, n.p.), and sustaining an “inverted relation” in which financial expansion appears autonomous, “in the way that even an accumulation of debts can appear as an accumulation of capital,” while an accumulation of data likewise appears as an accumulation of capital (Bellamy Foster 2010, n.p.).

Crucially, the AI-centred expansion within Silicon Valley is not merely a spontaneous outcome of market forces. It is politically and institutionally scaffolded through the state’s deep incorporation into the financial architecture of accumulation, illustrated by U.S. President Donald Trump’s early second term announcement of “a private sector investment of up to $500 billion to fund infrastructure for artificial intelligence, aiming to outpace rival nations in the [so-called] business-critical technology” (Holland 2025, n.p.). As Bellamy Foster argues of monopoly finance capitalism, “the role of the capitalist state was transformed,” with its function “as lender of last resort, responsible for providing liquidity at short notice … fully incorporated into the system,” including an explicit “‘too big to fail’ policy toward the entire equity market” (Bellamy Foster 2007, n.p.). Under these conditions AI takes on the character of a quasi-public investment object. Valuations are stabilized not only by private speculation but by expectations of state procurement, subsidies, and strategic industrial policy that underwrite forward claims even where immediate profitability remains thin.

Enclave Growth and Systemic Concentration: Financial and Industrial Implications

Baran and Sweezy’s third surplus absorption mechanism, disproportionate sectoral expansion, describes a pattern in which accumulation under monopoly conditions concentrates in a narrow enclave whose growth becomes detached from the trajectory of the broader economy. The claim is not the trivial one that sectors grow at different rates. It is that, under chronic surplus and limited outlets for profitable productive reinvestment, capital is repeatedly channelled into a small set of “leading” sectors that can absorb exceptional inflows through scale, market power, and institutional credibility.

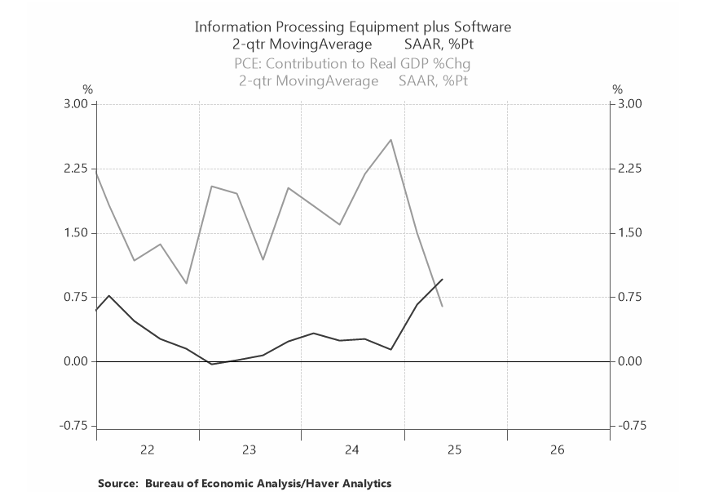

Once again, the Western approach to AI investment manifests this mechanism with unusual clarity. It is visible first in the increasingly top heavy structure of equity performance and valuation. As McGeever notes, “since the beginning of 2023, the S&P 500 composite benchmark ‘market cap’ index increasingly dominated by the ‘Mag 7’[vii] has gained 67%, more than double the ‘equal weight’ index’s 32%” (2025, n.p.). The enclave dynamic is then reproduced on the side of fixed investment. In 2025, analysts observed that AI related capital expenditure, proxied by information processing equipment and software plus data centre buildout, contributed an outsized share of measured GDP growth (Watts 2025). The St. Louis Fed similarly reports that “in the first quarter of 2025, the contribution of information processing equipment (IPE) to real GDP growth jumped to 0.90 percentage points, which is more than two standard deviations above its long run average” (Rubinton and Patro 2026, n.p.).

At the same time, the enclave character of AI is revealed by the widening gap between the capitalization of anticipated productivity gains and the limited success of realized implementation. MIT linked reporting captures this disjunction through the “GenAI Divide,” which separates widespread experimentation and piloting from sustained enterprise deployment and measurable productivity effects (Challapally, Pease, Raskar and Chari 2025). Whatever the limitations of the metrics, particularly the reduction of productivity measurement to GDP, which excludes unpaid labour, and oft-conflates value creation with financial and speculative activity (Ivković 2016), the substantive point nevertheless stands; Much adoption functions as a programmatic and reputational imperative, while effective integration remains uneven and insufficient to justify the scale of capital committed.

In monopoly capital terms, this gap is constitutive rather than incidental. Enclave expansion is compatible with weak generalized productivity precisely because profitability tests are deferred into the future, diffused across portfolios, and buffered by institutional supports rather than disciplined by realized returns. Sawyer captures the broader historical conditions, emphasizing rising industrial concentration across western countries and “shifts in the structure of production … away from manufacturing … to services, and notably industries of information technology” (2023, 545–65). AI intensifies this tendency by concentrating both valuation and investment in a sector whose promissory horizon can be sustained even when diffusion remains partial.

This disproportionate expansion has a determinate material geography. The AI enclave is not reducible to software. It is a composite complex spanning semiconductor fabrication and supply chains, hyperscale cloud infrastructure, data centre construction, grid and generation upgrades, and a surrounding ecosystem of contractors, consultants, integration vendors, and security and compliance industries. This buildout can absorb surplus across multiple adjacent sectors at once, producing the appearance of broad investment momentum while remaining tethered to the credibility of AI’s “promissory exuberance” (Desai 2026, 6-7). For that reason, the boom has the character of enclave led accumulation rather than generalized expansion. It concentrates demand in a corridor of upstream and downstream industries while leaving the wider economy’s productivity trajectory stubbornly weak (fig. 3).

|

|

Figure 3. AI-related capital expenditures (information-processing equipment and software) contributed more to GDP growth in 2025 than consumer spending (Renaissance Macro Research, 2025). |

Automation, Labour Markets, and Strategic Stability

Neoclassical and techno-optimist interpretations of the contemporary AI boom rest on a fundamental misdiagnosis. Faced with Solow’s paradox,[viii] which “provided the first evidence of the paradoxical low return of technological progress to productivity” (Capello, Lenzi and Perucca 2022, 166), such accounts routinely invoke the lagged productivity effects of computerization and the diffusion of the internet in the 1990s to argue that apparently weak returns will eventually resolve themselves. In doing so, however, they repeatedly treat scale as proof of success, mistaking unprecedented expenditure for demonstrated productivity gains. This misrecognition obscures a lesson already furnished by the dot-com boom. The underlying technology may endure, but the speculative investment cycle surrounding it can still signal a deeper structural problem. As I have argued elsewhere, “AI [as a technology] will survive, but the speculative bubble surrounding it is a sign of a deeper structural problem, the cost of which, when finally realized, will fall most heavily on the working class” (Goodell Ugalde, 2025a, n.p.).

Against this view, the contemporary AI investment regime is not merely a financial story about exuberant valuations. It is also a set of production technologies whose diffusion reshapes firm strategy, labour markets, and the macroeconomic conditions under which profits are made (Finio and Downie, 2024). AI therefore plays a dual role. It operates as a privileged outlet for surplus investment under conditions of weak productive returns, while simultaneously reorganizing production in ways that can intensify the very stagnation it is supposed to overcome. As a production technology, AI is introduced not as a neutral efficiency gain but as a capital intensive, labour displacing innovation. Its deployment requires large advances of fixed infrastructure in data centres, specialized chips, energy systems, and software integration, while compressing or eliminating labour across administrative, cognitive, and professional domains (Robbins and Van Wynsberghe 2022). Even where adoption yields local efficiencies, economy wide diffusion can produce perverse aggregate effects by accelerating competitive cost cutting and labour displacement faster than productivity benefits generalize.

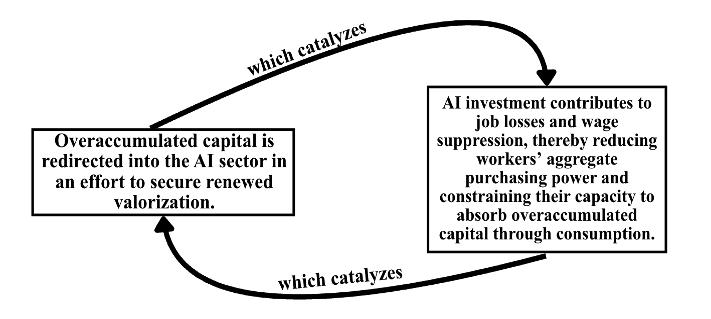

A dialectical contradiction thus follows: First, AI mediated automation can contribute to weaker economy wide dynamism by intensifying cost competition and concentrating gains in a narrow set of firms and sectors, thereby reinforcing secular stagnation. Second, because AI displaces workers and disciplines wages, and “there is clear evidence that recent automation, including AI has already led to job losses” (Aldred 2024), it suppresses aggregate purchasing power and deepens the realization problem. As Leo Winternitz (1949) puts it, the fact that commodities are useful “does not guarantee that they are saleable” (n.p.) in a way that realizes surplus value. As such, workers displaced or precarized through AI-driven restructuring do not constitute an expanding market for commodities. Their constrained consumption instead enlarges the mass of overaccumulated capital, which then feeds back into the stagnation the AI investment wave is ostensibly meant to overcome by revalorizing segments of that same surplus capital (see fig. 3).

|

|

Figure 3. The dialectical interaction between AI as constant capital and as a syphon for overaccumulated capital. |

This recursive dynamic is amplified by contemporary geopolitical constraints on outward displacement. Historically (in line with Luxemburg’s prior-explored thesis) overaccumulated capital sought temporary relief through spatial expansion. As Harvey notes, “if, for example, a crisis of localized overaccumulation occurs within a particular region or territory then the export of capital and labor surpluses to some new territory to start up new production would make most sense” (Harvey 2001, 23). Yet protectionism, export controls, and the fragmentation of global supply chains increasingly restrict these outlets. The U.S. tariff escalation, in which “in the space of four months January to April 2025 the average levy on imported goods rocketed from 2.5 percent to roughly 27 percent, the steepest hike (and highest level) since the 1920s” (Goodell Ugalde 2025b, n.p.), exemplifies the tightening of the external space once available for surplus absorption. As traditional outlets narrow, surplus funds are more readily recycled into domestic speculative circuits, further inflating AI valuations and reinforcing enclave patterns of accumulation.

With spatial displacement constrained, the market, in turn, leans harder on temporal displacement, and monetary conditions become decisive. Political pressure for rate cuts, along with the broader expectation that liquidity will be provided in moments of stress, encourages longer investment horizons and greater tolerance for loss making expansion (Kaye 2026). Cheap credit enables firms to roll over losses, maintain elevated valuations, and defer profitability tests without resolving underlying weaknesses. It does not restore productive momentum so much as postpone its reckoning by converting present stagnation into future obligations. This dynamic intensifies fragility by sustaining the belief that credit can generate returns without exposure to the “troubles and risks inseparable from its [productive] employment in industry” (Marx 1867, n.p.). In reality, it shifts those risks forward and outward.

When expectations finally tighten, the adjustment is typically abrupt. The withdrawal of credit precipitates rapid devaluation, layoffs, and consolidation (Harvey 2018). Losses are reorganized rather than evenly borne, and the burden falls predictably on workers through job loss, wage compression, pension volatility, and austerity pressures as public revenues weaken. The eventual crash of the AI bubble, on this view, would not demonstrate the failure of AI as a technology. It would mark the exhaustion of its capacity to function as a stabilizing outlet for surplus investment under stagnation.

Policy Recommendations: Managing Financial Concentration and Building Strategic Resilience

With the foregoing analysis in view, this research report recommends an integrated federal policy framework combining macroprudential oversight, active industrial policy, and strategic infrastructure governance. Although written for a Canadian audience, the underlying vulnerabilities are common across advanced Western economies confronting similar patterns of financial concentration and AI-led capital inflows. The objective is not to impede artificial intelligence development, but to ensure that AI does not operate primarily as a speculative absorber of surplus capital whose eventual repricing would transmit avoidable social, fiscal, and strategic instability across financial systems and the broader real economy.

Macroprudential Oversight of AI-linked Concentrations

A first pillar is macroprudential oversight of AI linked concentration risk. Regulators should require clear, decision useful disclosure of AI related equity and credit exposures across pension funds, major asset managers, and leveraged non bank financial institutions, with reporting formats intelligible to beneficiaries and worker representatives. This matters because concentration is no longer a marginal market feature. It is increasingly a defining condition of benchmarked returns. Reuters reports that since the beginning of 2023 the market cap weighted S&P 500, increasingly dominated by the “Mag 7,” gained 67 percent, more than double the 32 percent gain of the equal weight index (McGeever 2025). In such an environment, concentrated exposures become a systemic transmission channel, not merely a portfolio choice.

Further, disclosure should be paired with stress testing that models sharp repricing of major tech and AI linked assets and traces second order effects through collateral calls, liquidity pressures, credit tightening, and public revenue sensitivity. This emphasis aligns with the European Systemic Risk Board’s (ESRB) assessment that vulnerabilities in non bank financial intermediation can amplify stress, particularly via investment funds and interconnected market based channels (2025). It is also consistent with the Financial Stability Board’s (FSB) conclusion that leverage in non bank intermediation can materially amplify shocks and warrants stronger, more timely data collection alongside targeted tools, including measures addressing leverage, margining, and concentration where risks are acute (2025). For long horizon institutions, the case is strengthened by the OECD’s (2025) finding that the share of pension assets invested in equities increased in 2024, raising exposure to equity drawdowns and reinforcing the need to understand how concentrated index dynamics interact with retirement security and financial stability.

Conditioned credit and disciplined state guarantees

Further, monetary easing and public guarantees should not operate as unconditional support for AI linked balance sheets and valuations. A substantial literature on post crisis stabilization emphasizes that liquidity injections routed primarily through financial markets can raise asset prices while delivering limited traction on consumption and productive investment when private balance sheets are impaired and demand is weak.

For example, Stiglitz and Rashid demonstrate that the post 2008 policy mix of quantitative easing alongside fiscal retrenchment “offered little support for household consumption, investment, and growth,” while disproportionately enriching financial asset holders and inflating asset prices rather than restoring broad based expansion (Stiglitz and Rashid 2016). Neo-Keynesian work on debt driven slumps similarly concludes that when deleveraging and liquidity constraints dominate, policies that work directly through demand support are comparatively more effective than reliance on monetary expansion alone, since constrained agents cut spending and financial accommodation does not reliably translate into new real expenditure (Eggertsson and Krugman 2012). The policy implication is straightforward. Public support can be justified, including in downturn conditions, but it is most defensible when it is conditioned on verifiable contributions to productive capacity and strategic resilience rather than treated as a general backstop for speculative positioning.

Accordingly, where subsidized credit, guarantees, or industrial supports are extended to AI linked investment, access should be conditional on measurable outcomes such as additions to productive capability, security relevant infrastructure, or demonstrable public value rather than GDP alone. This implies constraining the use of subsidized credit for buybacks or purely reputational expansion, and tightening standards for debt instruments whose collateral value rests primarily on projected AI revenues that are not anchored in realized cash flows, given the volatility of promissory horizons. The goal is to limit dependence on finance-led stimulus that expands forward claims without strengthening the real economy that must ultimately validate those claims, and thus to reduce reliance on a fictitious “money [supply] that is thrown into circulation as capital without any material basis in commodities or productive activity” (Harvey 2018, 95).

Redirect surplus capital into socially necessary and security-relevant infrastructures

If surplus capital is searching for outlets, the state should steer it into investments that raise resilience and reduce strategic vulnerability, rather than allowing capital to default into speculative cycles. Energy and grid resilience is the binding constraint. The International Energy Agency (IEA) estimates that data centres accounted for about 1.5 percent of global electricity consumption in 2024, or roughly 415 TWh, and emphasizes that AI is a key driver of rapid demand growth. Belgium’s grid operator has warned that data centre connection requests have risen ninefold since 2022 and has floated consumption limits and dedicated capacity allocation to prevent speculative projects from tying up scarce grid space (Kacher, 2025). Directing investable surplus toward generation, transmission, interconnection, and flexibility therefore functions as strategic infrastructure policy that protects system reliability while avoiding capacity crowding that can impair other industrial and public priorities.

Beyond energy, redirecting surplus toward public housing, public transit, and associated low-carbon infrastructure strengthens resilience in the real economy by expanding durable productive capacity while absorbing labour. In doing so, it mitigates pressures of overaccumulation by increasing consumer purchasing power and stabilizing the conditions of social reproduction that underpin fiscal and state capacity. This logic is consistent with John Maynard Keynes’s (1936) argument in which he contends that when private investment is insufficient to sustain full employment, “a somewhat comprehensive socialisation of investment will prove the only means of securing an approximation to full employment” (ch. 24). As Keynes points out, the issue is not the suppression of private enterprise but the stabilization of aggregate demand through public direction of investment when expectations are weak and capital is reluctant to commit to productive expansion. In such conditions of slack, public infrastructure spending raises output and employment directly, while also improving the long-term productive capacity of the economy.

Public compute and data governance as strategic infrastructure

A significant share of the AI boom is sustained by private control over computers and data, which turns capability into scarcity and scarcity into market power. Desai argues that Silicon Valley’s training paradigm “presume[s] the availability of vast quantities of data” and has therefore pushed a drive to digitize and appropriate “every form of information without compensation to creators,” enabling firms to “appropriate, monetize and monopolise” AI processes as rent streams (2026, 11). Concentrated control over frontier-scale tech and proprietary model access then reinforces speculative expectations, because national and organizational capability appears to hinge on a small set of firms whose revenues are tied to platform dependence and whose valuations are sustained by the promise of exclusive capacity rather than demonstrated, widely diffused productivity gains.

A resilience-oriented response is to treat technology and data as strategic infrastructure with public options that reduce lock-in. Desai’s core empirical contrast is that China’s DeepSeek[ix] achieved competitive performance without the same data-extensive, capital-heavy model, using approaches such as “synthetic data” and “distillation,” and then released R1 as open source (2026, 11). Building on that logic, public computers for universities, hospitals, and small firms would widen access to advanced capacity without routing adoption through a handful of cloud and model gatekeepers. Publicly governed data trusts, with clear privacy and security rules, would enable research and deployment without monopoly enclosure or forced data surrender. Finally, sustained support for open-source AI ecosystems would reduce proprietary chokepoints and lower geopolitical and procurement risk, because capability would be anchored in reproducible public infrastructure and shared tooling rather than in bubble-sensitive private valuations (WEF, 2019).

Conclusion: Embedding AI Within a Resilient Political Economy

The AI investment surge should not be understood merely as technological exuberance or the spontaneous maturation of a general purpose innovation. It is more accurately interpreted as a structurally conditioned response to overaccumulation amid decades of secular stagnation across the West, in which capital, confronted with limited profitable outlets in productive activity, reconstitutes itself around promissory horizons sustained by credit expansion, corporate concentration, and active state scaffolding (Carlos Bresser-Pereira 2024). In this configuration, AI functions simultaneously as a production technology and as a financial object, absorbing surplus while multiplying forward claims on productivity that remain only partially realized. The result is enclave-led growth that coexists with weak generalized dynamism and rising systemic interdependence.

This dynamic does not imply that AI lacks transformative potential. It does imply that the present scale and structure of western investment exceed what can presently be validated through realized surplus value and broad-based productivity gains. When accumulation is stabilized primarily through temporal deferral, expectations become a macroeconomic variable. The tightening of liquidity, geopolitical shocks, or a repricing of growth narratives can therefore transmit instability across pensions, labour markets, public finances, and critical infrastructures. In such moments, adjustment predictably falls unevenly, with workers and public institutions bearing losses while surviving firms consolidate strategic control.

A resilient strategy must therefore refuse the false choice between technological enthusiasm and technological rejection. The task is to embed AI development within a macroprudential, industrial, and infrastructural framework that strengthens the real economy rather than amplifying speculative concentration. By conditioning credit, widening access to strategic technology and energy capacity, and redirecting surplus toward socially necessary investment, Western governments can reduce dependence on enclave-driven accumulation and credit-fueled deferral. In doing so, they would address not only the volatility and security risk of the current AI cycle, but the deeper structural constraints that made such a cycle predictable in the first place.

References:

Aldred, J. S. Post-Growth, Secular Stagnation and the Rise of AI: Can Mass Unemployment Be Avoided? SSRN Scholarly Paper. Rochester, NY: Social Science Research Network, 2024.

Andreessen, Marc. “The Techno-Optimist Manifesto.” Andreessen Horowitz (a16z), October 16, 2023.

Arrighi, Giovanni. “Spatial and Other ‘Fixes’ of Historical Capitalism.” In Global Social Change: Historical and Comparative Perspectives, 202–224. London: Palgrave Macmillan, 2006.

Ashley, Richard K. “The Poverty of Neorealism.” International Organization 38, no. 2 (1984): 225–286.

Baran, Paul A., and Paul M. Sweezy. Monopoly Capital: An Essay on the American Economic and Social Order. New York: Monthly Review Press, 1966.

Bieler, Andreas, Sümercan Bozkurt, Max Crook, Peter S. Cruttenden, Ertan Erol, Adam David Morton, Cemal Burak Tansel, and Elif Uzgören. “The Enduring Relevance of Rosa Luxemburg’s The Accumulation of Capital.” Journal of International Relations and Development 19, no. 3 (2016): 420–447.

Brynjolfsson, Erik, Daniel Rock, and Chad Syverson. “Artificial Intelligence and the Modern Productivity Paradox: A Clash of Expectations and Statistics.” NBER Working Paper No. 24001. Cambridge, MA: National Bureau of Economic Research, 2017.

Bukharin, Nikolai. Historical Materialism: A System of Sociology. London: Routledge, 2013.

Caballero, Ricardo J. Speculative Growth and the AI “Bubble.” NBER Working Paper No. 34722. Cambridge, MA: National Bureau of Economic Research, 2026.

Cadwalladr, Carole. “‘Capitalism Is Dead. Now We Have Something Much Worse’: Yanis Varoufakis on Extremism, Starmer, and the Tyranny of Big Tech.” The Observer, September 24, 2023.

Capello, Roberta, Camilla Lenzi, and Giovanni Perucca. “The Modern Solow Paradox: In Search for Explanations.” Structural Change and Economic Dynamics 63 (2022): 155–168.

Bresser-Pereira, Luiz Carlos. “Secular Stagnation, Low Growth, and Financial Instability.” International Journal of Political Economy 48, no. 1 (2019): 21–40.

Challapally, A., C. Pease, R. Raskar, and P. Chari. The GenAI Divide: State of AI in Business 2025. Cambridge, MA: MIT NANDA Project, Massachusetts Institute of Technology, 2025.

Clarke, Simon. “The Marxist Theory of Overaccumulation and Crisis.” Science & Society 54, no. 4 (1990): 442–467.

Clark, Brett, John Bellamy Foster, and R. Jamil Jonna. “The Contagion of Capital: Financialized Capitalism, COVID-19, and the Great Divide.” Monthly Review 72, no. 8 (January 2021). https://monthlyreview.org/2021/01/01/the-contagion-of-capital/.

Cochrane, John H. “Financial Markets and the Real Economy.” 2005.

Crafts, Nicholas. “Artificial Intelligence as a General-Purpose Technology: An Historical Perspective.” Oxford Review of Economic Policy 37, no. 3 (2021): 521–536.

Cutrone, Chris. “The End of the Gilded Age: Discontents of the Second Industrial Revolution Today.” Platypus Review 102 (2017).

Dawson, Michael, and John Bellamy Foster. “The Tendency of the Surplus to Rise, 1963–1988.” In The Economic Surplus in Advanced Economies, 42–70. Cheltenham: Edward Elgar, 1992.

Kaye, Danielle. “Trump Adviser Calls for Fed Economists to Be ‘Disciplined.’” BBC News, February 18, 2026. https://www.bbc.com/news/articles/clygwv38k1xo.

Desai, Radhika. “DeepSeek Upends Silicon Valley’s Sci-Fin-Fi Business Model.” International Critical Thought (2025): 1–19.

Eggertsson, Gauti B., and Paul Krugman. “Debt, Deleveraging, and the Liquidity Trap: A Fisher–Minsky–Koo Approach.” Quarterly Journal of Economics 127, no. 3 (2012): 1469–1513.

European Securities and Markets Authority. EU Non-Bank Financial Intermediation Risk Monitor 2025. Paris: European Securities and Markets Authority, 2025.

Federal Reserve. “Statement by Federal Reserve Chair Jerome H. Powell.” YouTube video, May 2026.

Feldman, Benjamin, and John Bellamy Foster. “Baran and Sweezy’s ‘Monopoly Capital,’ Then and Now.” Monthly Review 67, no. 6 (November 2015). https://monthlyreview.org/2015/11/01/baran-and-sweezys-monopoly-capital-then-and-now/.

Financial Stability Board. Leverage in Nonbank Financial Intermediation: Final Report. Basel: Financial Stability Board, July 9, 2025.

Finio, M., and A. Downie. “How Is AI Being Used in Manufacturing?” IBM Think, 2024.

Foster, John Bellamy. “The Financialization of Capitalism.” Monthly Review 58, no. 11 (2007).

Foster, John Bellamy. “The Financialization of Accumulation.” Monthly Review 62, no. 5 (2010).

Goodell Ugalde, Elliot. “The AI Bubble Isn’t New—Karl Marx Explained the Mechanisms Behind It Nearly 150 Years Ago.” MR Online. Originally published in The Conversation, November 30, 2025.

Goodell Ugalde, Elliot. “Trump’s Tariff Barrage Isn’t Import-Substitution: It’s Protectionism on the Fly.” Centre for International and Defence Policy, Queen’s University, May 30, 2025.

Goodell Ugalde, Elliot. “In Defence of Marx’s Labour Theory of Value: Vancouver’s Housing ‘Crisis.’” Assessment 353, no. 6296 (2016): 288–291.

Hardcastle, E. “The Falling Rate of Profit.” Socialist Standard, June 1960.

Harvey, Bo. 2026. “A Kind of Discursive Bridge Between Economics and Marxism.” Monthly Review, review of Value and Crisis: Essays on Marxian Economics in Japan, by Makoto Itoh.

Harvey, David. “Globalization and the Spatial Fix.” Geographische Revue 2, no. 3 (2001): 23–31.

Harvey, David. The Limits to Capital. London: Verso, 2018.

Holland, Steve. “Trump Announces Private-Sector $500 Billion Investment in AI Infrastructure.” Reuters, January 21, 2025.

International Energy Agency. Energy and AI. Paris: International Energy Agency, 2025. https://www.iea.org/reports/energy-and-ai.

Ivković, Ana Fotea. “Limitations of GDP as a Measure of Progress and Well-Being.” Ekonomski Vjesnik / Econviews 29, no. 1 (2016): 257–272.

Jessop, Bob. “Spatial Fixes, Temporal Fixes and Spatio-Temporal Fixes.” In David Harvey: A Critical Reader, 142–166. London: Blackwell, 2006.

Kacher, Alban. “Belgium Mulls Energy Limits for Power-Hungry Data Centres as AI Demand Surges.” Reuters, October 22, 2025.

Keynes, John Maynard. The General Theory of Employment, Interest and Money. London: Macmillan, 1936.

Luxemburg, Rosa. The Accumulation of Capital. Translated by Agnes Schwarzschild. London: Routledge & Kegan Paul, 1963.

Luxemburg, Rosa. The Accumulation of Capital: An Anti-Critique. Translated by Nicholas Gray. London: Routledge & Kegan Paul, 1972.

Marx, Karl. Capital: A Critique of Political Economy. Vol. 1. Translated by Ben Fowkes. London: Penguin Classics, 1976.

Marx, Karl. Capital: A Critique of Political Economy. Vol. 3. Translated by David Fernbach. London: Penguin Classics, 1981.

Marx, Karl. “Chapter Thirty-One: Genesis of the Industrial Capitalist.” Marxists Internet Archive. https://www.marxists.org/archive/marx/works/1867-c1/ch31.htm.

Mattick, Paul. “Marx’s Crisis Theory.” In Economic Crisis and Crisis Theory. Marxists Internet Archive, 1974.

McGeever, Jamie. “Is US Stock Rally near ‘Mag 7’ Turning Point?” Reuters, July 28, 2025.

OECD. Pension Markets in Focus 2025. Paris: OECD Publishing, 2025.

Ozturkcan, Selcen, and Ayşe Aslı Bozdağ. “Responsible AI in Marketing: AI Booing and AI Washing Cycle of AI Mistrust.” International Journal of Market Research 67, no. 6 (2025): 696–722.

RenMac: Renaissance Macro Research. “So Far This Year, AI Capex Has Added More to GDP Growth Than Consumers’ Spending.” X (Twitter), July 30, 2025.

Robbins, Scott, and Aimee Van Wynsberghe. “Our New Artificial Intelligence Infrastructure: Becoming Locked into an Unsustainable Future.” Sustainability 14, no. 8 (2022): 4829.

Rubinton, Hannah, and Bontu Ankit Patro. “Tracking AI’s Contribution to GDP Growth.” On the Economy Blog, Federal Reserve Bank of St. Louis, January 12, 2026.

Schwab, Klaus. The Fourth Industrial Revolution. New York: Crown Currency, 2017.

Sciuk, Christian, Simon Engert, Maren Gierlich-Joas, and Thomas Hess. “How Companies Navigate the (Un)Charted Waters of Digital Transformation.” California Management Review 68, no. 1 (2025): 5–31.

Solow, Robert M. “We’d Better Watch Out.” New York Times Book Review, July 12, 1987.

Stiglitz, Joseph E., and Hamid Rashid. “What’s Holding Back the World Economy?” Project Syndicate, February 8, 2016.

Sweezy, Paul M. The Theory of Capitalist Development: Principles of Marxian Political Economy. New York: Monthly Review Press, 1942.

Tranjan, Ricardo. The tenant class. Between the Lines, 2023.

Watts, Randy. “Capital Spending as the Key Market Driver?” Forbes, August 14, 2025.

Winternitz, Joseph. “The Marxist Theory of Crisis.” Modern Quarterly 4, no. 4 (1949).

Whiting, Kate, and HyoJin Park. “This Is Why ‘Polycrisis’ Is a Useful Way of Looking at the World Right Now.” World Economic Forum, March 7, 2023.

World Bank. Households and NPISHs Final Consumption Expenditure (Current US$). World Development Indicators database. Washington, DC: World Bank, 2026.

World Economic Forum. Guidelines for AI Procurement. Geneva: World Economic Forum, September 2019.

Youvan, Douglas C. “The Dot AI Bubble: Analyzing the Potential for an AI Industry Collapse and Its Economic Implications.” 2025.

[i]Elliot Goodell Ugalde is a PhD candidate in Political Studies at Queen’s University specializing in international political economy and the political economy of technological change. His research focuses on financialization, monopoly capital, and the systemic economic implications of emerging technologies, particularly artificial intelligence.

His peer-reviewed work has appeared in journals including Constellations, Social Policy & Administration, the International Journal of Law, Ethics and Technology, and Policy Design and Practice. He is also co-editor of the special issue “Territorial Rights: New Directions and Challenges” in the Critical Review of International Social and Political Philosophy. His policy and public scholarship has been published in outlets such as The Conversation, Monthly Review Online, and the National Observer.

[ii]The author thanks Wayne S. Cox (Centre for International and Defence Policy, Queen’s University), Radhika Desai (Geopolitical Economy Research Group, University of Manitoba), Natalie Braun (York University), and Thomas Marois (Public Banking Project, McMaster University) for valuable conversations and intellectual engagement related to the political economy of artificial intelligence and contemporary capitalism. Any errors or omissions remain the author’s responsibility.

[iii]Spatio-temporal displacement refers to capitalism’s tendency to temporarily resolve crises of overaccumulation by shifting surplus capital across space (to new regions or markets) or forward in time (through credit, debt, or long-term infrastructural investment), thereby deferring but not eliminating underlying contradictions (Jessop 2006).

[iv]Overaccumulation refers to a condition in capitalism in which surplus capital and labour cannot find sufficiently profitable outlets for investment, leading to stagnation, crisis, or the devaluation and destruction of capital (Clarke 1990).

[v]Secular stagnation is the condition in which an economy experiences persistently weak demand, low growth, and chronically low interest rates over the long term, even in the absence of cyclical recession.

[vi]Variable capital is the portion of capital advanced by a capitalist to purchase labor power (Marx 1976).

[vii]The “Mag 7” refers to the seven dominant U.S. technology corporations (Apple, Microsoft, Alphabet, Amazon, NVIDIA, Meta, and Tesla) that dominate AI development, infrastructure, and capital investment, and whose market power is increasingly tied to artificial intelligence technologies.

[viii]Solow’s paradox refers to Robert Solow’s (1987) observation that rapid advances in computer and information technology did not appear to produce corresponding gains in measured productivity growth.

[ix]DeepSeek is a Chinese artificial intelligence company that develops large language models and open-source AI systems designed to compete with leading Western AI platforms.