ESG Policies

1. Please provide your ESG-related policies. Please provide a formal statement of your ESG-related policies if you have one.

Fiera Capital’s Sustainable Investing Policy outlines the firm’s approach to integrating sustainability risks and opportunities into investment processes and highlights the many benefits of increasing our knowledge of companies in which we invest, better controlling the risk of our portfolios and helping companies improve over the long term. The policy also provides a blueprint for “active ownership,” which includes the tactical use of proxy voting rights and engagement with the management of companies in which the firm invests in order to address ESG issues and affect positive change.

The Firm’s ESG-related policies are reviewed annually and updated as needed to ensure that they are effective and in line with best practices.

Fiera Capital’s Sustainable Investment Policy and Proxy Voting Guidelines enclosed.

2. Are sustainable investing and ESG factors integrated into your investment process and portfolio management decisions? If yes, please provide details.

ESG Integration

ESG factors are fully integrated into the fundamental investment decision-making of the IFI team, whose investment processes reflect the belief that organizations that successfully manage ESG factors create more resilient businesses and are better positioned to deliver sustainable value over the long term. When an area of concern is identified, the team assesses the potential impact it may have on the financial performance of the issuer and, if deemed material, adjusts its assessment of the return required to compensate investors for the additional risk. Materiality is assessed using a sector-specific approach – the team leverages frameworks such as the Sustainability Accounting Standards Board (“SASB”) materiality map as well as the Fiera Materiality Map to identify ESG factors most likely to impact financial performance within each industry. For example, environmental risks such as carbon intensity and transition plans are prioritized in energy and utilities, while governance structures and board diversity are more material for financials. This mapping ensures that ESG analysis is focused on the factors most relevant to each issuer’s risk profile and business model. The team believes that it can gain a competitive edge through better understanding how traditional financial and non-traditional, non-financial factors can influence a company’s costs, risks, opportunities, and competitive advantages; therefore, every company research report produced by the team includes a formal ESG section highlighting both positive and negative ESG aspects identified during the research process. ESG-related conclusions feed directly into the valuation and can impact portfolios in multiple ways, including flagging certain issuers for additional monitoring, avoidance of new issues from certain issuers, or partial/full divestment of existing positions.

Monitoring & Review

ESG risks are integrated into the team’s portfolio management tools, allowing exposures to be monitored at both a total portfolio level as well as for individual issues on an ongoing basis. The Fiera Sustainable Investments team maintains a proprietary ESG database that includes historical and current Fiera ESG scores, carbon metrics, and engagement records for Canadian corporate issuers, allowing the team to view and analyze historical trend data. The team uses business intelligence tool to manipulate this data and generate various reports which our used both internally and for client reporting. This database is updated continuously as new information becomes available, including outcomes from ESG engagements, updates to internal ESG assessments, and changes in issuer disclosures. The Sustainable Investments team is the owner of the ESG database, its infrastructure, and the scoring process, and maintains independence from the portfolio management teams to ensure adequate governance. The Fiera Fixed Income ESG Subcommittee provides a forum in which the IFI team can provide feedback on ESG-related matters such as scoring, rating adjustments, overrides, any process changes, and discuss any other topical subjects (e.g. the increasing acceptance of Nuclear as a transition energy).

One of the key responsibilities of the Sustainable Investments team is the maintenance of the Fiera ESG score. As of 2024, Fiera’s external ESG data provider covered only ~62% of Canadian corporate names; to overcome this challenge, the IFI team in cooperation with the Sustainable Investments team has developed an internal scoring methodology to address gaps and allow the team to have ratings for all issuers in its coverage universe. At the time of writing, the internal database has ESG ratings for over 300 corporate and government names. The starting point for the Fiera ESG score is data from an external ESG data provider who provides baseline ratings, controversy flags, and raw data points. Where there are gaps, sector averages are used and then adjusted by the Fixed Income ESG Subcommittee to ensure consistency and relevance. Adjustments are limited to +/- 2 notches for each sub-component, ensuring consistency while allowing for subjectivity when external data is incomplete or misaligned with issuer realities. For unrated issuers, global sector averages are used and similarly adjusted.

At a firm level, Fiera Capital’s Global Sustainable Investing Committee reviews the practices and initiatives relating to ESG matters and oversees their development in line with market and regulatory expectations. The Committee includes key professionals and thought leaders from different business functions and regions across the organization. Collectively, they implement the firm’s strategic objectives related to sustainable investing.

3.a. Are you a signatory to the UNPRI?

Yes, Fiera Capital has been a Signatory of the United Nations Principles for Responsible Investment (UNPRI) since 2009.

3.b. If you are signatory to other coalitions, please list them.

Fiera Capital promotes sustainable investing through our participation in collaborative initiatives and by adhering to the firm’s established codes and policies. We believe that an integral part of our role as a responsible investor is through active contribution and collaboration with other players in the investment value chain to further develop the field. Accordingly, we have endorsed or signed onto several relevant standards and statements and are active members and signatories of various networks and sustainable investing initiatives. As well, we recognize and adhere to several responsible business codes of conduct, along with internationally recognized standards for due diligence and reporting.

We also frequently engage with external thought leaders, such as corporate social responsibility and impact investing experts to broaden our perspectives, improve our understanding of key topics, and complement our internal research. We have participated in or presented on several ESG expert panels and conferences and published several ESG-focused white papers.

The firm’s personnel are involved in numerous activities and have been invited as guest speakers to address sustainable investing. Furthermore, the firm’s personnel have been recognized by numerous industry organizations.

In 2025, we participated in various sustainable investing initiatives, industry associations, and working groups, including the following:

Better Buildings Partnership (BBP) Climate Commitment (2022): Fiera Real Estate UK joined the Better Buildings Partnership (BBP) as of October 2022 and has signed up to the BBP’s Climate Commitment. The BBP Climate Commitment acknowledges the transformation that is required across the real estate sector to deliver net zero buildings by 2050. The aim of the Commitment is to: leverage collaborative and tangible, strategic action on climate change, increase transparency and accountability enabling the market to operate and compete effectively, and provide clear client demand for net zero assets, driving the industry to respond.

Canadian Coalition for Good Governance (CCGG) (2014): CCGG promotes good governance practices among public companies in Canada, with a strong focus on independent board members of corporations. CCGG is increasingly focusing on environmental and social factors when engaging with board members. This relationship is beneficial to Fiera Capital, as it allows the firm to identify priorities related to ESG issues and work alongside other key industry players to promote both active ownership and identify potential improvements in governance and disclosures of ESG issues.

Canadian Fixed-Income Forum (CFIF) (2018): CFIF is a group set up by the Bank of Canada to facilitate the sharing of information between market participants and the Bank on the Canadian fixed-income market. An ESG committee has been created by CFIF and several other sub-committees and working groups were then created to work and issue recommendations on several themes and issues. Members of Fiera Capital have created and chaired a working group on ESG data which seeks the betterment of ESG disclosures by Canadian Issuers through collaborative and direct engagement.

CDP (2022): We are a signatory to the CDP, a project that aims to collect and share information on greenhouse gas emissions and climate change strategies.

Climate Action 100+ (2022): Fiera Capital is a member of the Climate Action 100+ investor engagement initiative, which addresses climate change with the world’s largest corporate emitters of greenhouse gases. As a member of this initiative, we participate in engagement activities centered on key goals: companies reducing their greenhouse gas emissions, implementing a strong governance framework that clearly articulates the board’s accountability and oversight of climate-related matters, and improving their climate-related disclosures. Our engagement efforts are underway, targeting Canadian energy issuer(s) on the Climate Action 100+ list that operate in Canada.

Climate Engagement Canada (CEC) (2023): In 2023, we became a member of Climate Engagement Canada (CEC), a finance-led initiative that drives dialogue between the financial community and corporate issuers to promote a just transition to a net zero economy. CEC focuses on select Toronto Stock Exchange-listed companies that are strategically engaged for the alignment of expectations on climate risk governance, disclosure, and the transition to a low-carbon economy in Canada. CEC’s Focus List companies have been identified as the top reporting or estimated emitters on TSX and/or with a significant opportunity to contribute to the transition to a low-carbon future and become a sectoral and corporate climate action leader in Canada. These firms operate across the Canadian economy in the oil and gas, utilities, mining, agriculture and food, transportation, materials, industrials and consumer discretionary sectors. Since joining the initiative, we have joined a total of nine engagement collaboration groups.

Global Real Estate Sustainability Benchmark (GRESB) (2019): GRESB is the most recognized global ESG benchmark for real assets. Over 100 institutional investors including Fiera Capital, representing approximately USD$22 billion in assets under management, use GRESB data to monitor their investments and make decisions that lead to a more sustainable industry.

Impact Management Norms by Impact Frontiers (2020): Formerly known as the Impact Management Project, the framework was initially backed by many foundations, asset owners and asset managers around the world, and aimed to provide a framework for impact measurement. This framework is currently used in our Global Impact Fund, which was launched in 2020.

Net Zero Asset Managers (NZAM) (2021): Fiera Capital Corporation joined the Net Zero Asset Managers initiative (NZAM) in 2021. Despite recent changes with regards to NZAM, we remain dedicated to working proactively towards the goal of reaching net-zero greenhouse gas emissions by 2050 or sooner, supporting efforts to limit global warming to 1.5ºC. Significant effort was put into defining the methods and metrics required to produce credible and robust targets. We believe our approach is consistent with delivering a fair share of the 50% global reduction in CO2 emissions by 2030.

Responsible Investment Association (RIA) (2016): The RIA is Canada’s membership association for Responsible Investment. Members believe that integrating Environmental, Social and Governance factors into the selection and management of investments can provide superior risk-adjusted returns and positive societal impact.

Sustainability Accounting Standards Board (SASB) (2020): SASB is a framework with growing global recognition. As an official supporter since 2020, we promote the standard internally, and it is used by an increasing number of our investment teams across the firm.

Task Force on Climate-Related Financial Disclosures (TCFD) (2022): We are an official supporter of TCFD. The task force’s recommendations provide a foundation for climate-related financial disclosures for all companies, encouraging them to report on the climate-related risks and opportunities most relevant to their particular businesses. In 2024, the IFRS Foundation took over the responsibilities from TCFD. The IFRS S2 standards are intended to replace the TCFD as the global climate reporting baseline.

UK Stewardship Code (2022): Fiera Capital has been a signatory to the UK Stewardship Code since 2022. Signatories of the UK Stewardship Code are required to annually report on their stewardship policies, processes, activities, and outcomes for a 12-month reporting period, setting a high stewardship standard.

UN PRI Collaborative Sovereign Engagement on Climate Change (2025): A PRI initiative that enables investor signatories to support governments to mitigate climate change, including supporting countries to fulfill their Paris Agreement-related comments, where applicable. Fiera Capital was selected to participate in the initiative in 2025.

Swiss Sustainable Finance (SSF) (2025): SSF is Switzerland’s leading association in the field for sustainable finance that brings together over 200 members and partners including asset managers, institutional asset owners, banks and other organizations committed to sustainability in finance. Fiera joined the SSF in 2025.

3.c. Indicate any other international standards, industry guidelines, reporting frameworks, or initiatives that guide your responsible investing practices.

Please see question 3b)

4. Please describe how ESG oversight and integration responsibilities are structured at your firm, including the process for escalation of key ESG issues. Also, if applicable, describe how responsible investment objectives are incorporated into individual or team employee performance reviews and compensation mechanisms.

Governance and oversight of our sustainable investing practices is a shared responsibility at Fiera Capital, involving various business divisions and functions to ensure we continue to enhance our capabilities in the years to come.

Global Sustainability Committee

Our business-wide body responsible for steering the global sustainability strategy. The Committee is responsible for overseeing the implementation of the company’s sustainable investing as well as its corporate sustainability strategies.

Sustainable Investing: The Committee reviews practices and initiatives relating to ESG matters and oversees both strategy development, in line with the market and regulatory expectations. Included within the Committee’s responsibilities is the creation of a climate-focused strategy, as well as strategic oversight of the integration of climate-related risks and opportunities by portfolio managers into the evaluation of potential investments.

Corporate Sustainability: The Committee is responsible for overseeing and driving the development of our sustainability strategy and ensuring that our business operations have a positive environmental and social impact.

The committee members are as follows:

- Executive Director, Global Chief Legal Officer and Corporate Secretary (Chair)

- Executive President and Chief Investment Officer of Public Markets

- Chief Investment Officer and Head of Private Markets Solutions

- Head of Sustainable Investing – Public Markets

- Head of Sustainable Investing – Private Markets

Sustainable Investing Team

The Sustainable Investing (“SI”) team is responsible for overseeing the implementation of Fiera Capital’s Sustainable Investing strategy by partnering with all investment teams. They serve as a center of sustainability excellence and a resource to promote continuous improvement in ESG integration across all our investment strategies. Together, they seek to provide transparency to our clients and ensure that Fiera Capital complies with applicable regulations. They actively communicate with the Global Sustainability Committee to share ESG information and seek approvals for policy positions and collaborative initiatives.

Investment Teams

The investment teams are accountable for implementing their own ESG integration process in a way that best suits their investment style and asset class.

Employee Performance Reviews and Compensation Mechanisms

Some of our resources, such as our Sustainable Investing team members, have incentives linked to the delivery of sustainable investing projects and objectives as part of their remuneration.

Similarly, some investment teams in our Private Markets division have sustainable investing-focused personal objectives linked to financial remuneration. For instance, our real estate investment teams have objectives linked to the achievement of certain GRESB points thresholds.

It is our belief that material sustainability factors affect the performance of the companies/issuers in which we invest, and that sustainability integration can therefore result in a better performance. While our investment teams and portfolio managers are mainly compensated on the performance of their strategies, our investment teams are indirectly compensated on their ability to manage these risks. We believe this incentivizes and motivates the investment team to consider sustainability-related risks.

5. How do you obtain ESG information/data (e.g. public information, third party research, reports and statements from the company, direct engagement with the company)? Please provide specific details of what information is obtained from each source, and how this information is acquired.

The analysis of ESG factors draws from diverse sources such as company disclosures, management discussions, public information, news sources, and data from external ESG research providers such as MSCI ESG and Bloomberg. The investment team, in collaboration with the Sustainable Investing team, has developed the Fiera ESG Score, allowing the team to have E, S, G, and Overall ESG Scores for over 300 Canadian corporate and government names. The Fiera ESG Score is based on publicly available ESG scores by MSCI ESG, which form the fundamental basis of issuer ESG ranking methodology across the Canadian corporate universe.

6. What channels do you use to communicate ESG-related information to clients and/or the public? Do you produce thought leadership (written reports and publications)? If so, is the information available to the public? Please provide links, if applicable.

Depending on the strategy, Fiera Capital provides client specific reporting on a quarterly basis. At the firm level, Fiera Capital produces on an annual basis the following reports: Sustainability Report, Climate Report and UK Stewardship Code.

Fiera Capital and its affiliates (where applicable) report on ESG and sustainable investing related progress. Fiera Capital’s UN PRI Transparency Report, which describes our initiatives and progress during the year as well as expected activities for the year to come, is produced annually and is available to our clients and beneficiaries upon request. Additional ESG related information, such as carbon intensity reporting and engagement reporting are also available to clients. The below reports can be made available to clients, as well as the potential to customize reports that incorporate ESG metrics that are important to a client:

- Extended Portfolio Summary Reports: generated using MSCI ESG, the report shows overall scores between portfolio and reference benchmark. It also provides high-level metrics on carbon footprint and controversy risk within the portfolio.

- Proxy Voting Results (for equity mandates only): generated using proxy voting results from ISS. We can provide greater details on votes executed over a specified period. For example; percentage votes against or for management, number of votes by proposal categories, etc.

- Climate Risk Reports: Generated using MSCI ESG, these reports provide transparency into portfolios' climate-related risks and opportunities according to the recommendations from the Task Force on Climate-related Financial Disclosures (TCFD). This report combines both current exposure climate data and forward-looking metrics.

- Carbon Metrics and Attribution Reports: Using data from MSCI ESG, we have built our own customized carbon metrics and attribution reports that compare carbon footprint of a portfolio against its reference benchmark. The attribution report helps identify where the difference in total weighted average carbon intensity is coming from. For example, is it due to sector allocation (allocation to sectors that are less carbon intensive) and/or security selection (within a sector, does the portfolio manager choose companies that are less carbon intensive than their peers)?

Furthermore, additional ESG-related information may also be made available to clients and beneficiaries upon request.

In addition, we regularly produce thought leadership pieces and reports on specific ESG themes and/or investment strategies available on our website

7. Do you have periodic reviews of your ESG process/approach to assess its effectiveness? What are the results? What would cause you to disregard ESG issues in your investment/analysis decisions?

The Firm’s ESG-related policies are reviewed annually and updated as needed by our Sustainable Investing Team to ensure that the policies are effective and in line with best practices.

UN PRI performs an annual assessment on our fulfilment of the six principles of sustainable investing. Our latest scores in 2025 reflect the collective efforts of every area within our firm in ESG concerns.

Climate

8. Describe how you identify, assess, and manage climate-related risks, and whether climate-related risks and opportunities are integrated into pre-investment analysis.

Environmental, social and governance (ESG) factors are integrated into the fundamental investment decision-making process of the Integrated Fixed Income strategy, whose investment processes reflect the belief that organizations that successfully manage ESG factors create more resilient businesses/assets and are better positioned to deliver sustainable value over the long term. The team takes a comprehensive approach to sustainable investing by combining ESG factors into their corporate credit research framework. When the team believes there could be a material impact on the business or financial profile of an issuer due to ESG concerns, it is factored into the assessment of the issuer’s securities and the evaluation of the required returns needed to compensate for the additional risk.

When the team believes there could be a material impact on the business or financial profile of the issuer it is factored into the assessment of the issuer’s securities, or the team modifies its judgement on the required returns to compensate for these additional risk factors. For example, for climate-related risks, the team is of the view that climate change related risks are becoming increasingly important in fundamental analysis due to the potential material impacts these risks may pose to companies’ long-term value prospects.

The team breaks down climate related risks as follows:

- Transition risks: transition risks are often easy to identify and are assessed using the team’s internal credit analysis as well as ESG data from external providers. According to the UN PRI’s “Inevitable Response” document, certain sectors are more exposed to transition risks than others, and higher risk companies often lag their peers in terms of carbon emissions (higher carbon intensity) as well in metrics measuring preparedness and transition planning.

- Physical risks: physical risks are more difficult to identify and monitor – the team is aware of the development of tools to better capture the potential impact on portfolio returns; however, these still need to be refined. When the team believes there could be a material impact on the business or financial profile of an issuer due physical risk concerns, it is factored into the assessment of the issuer’s securities and the team modifies their judgement on the required returns to compensate for the additional risk factors

The IFI team remains deeply committed to integrating climate-related considerations into our investment process. Our approach is grounded in issuer-level ESG analysis, which includes evaluating transition plans, emissions data, and progress toward climate goals. Every issuer in the portfolio is scored using our proprietary Fiera ESG Score, which covers over 300 Canadian corporate issuers and governments. This scoring framework incorporates environmental metrics such as Scope 1 and 2 emissions, carbon intensity, and transition readiness. Analysts have the flexibility to adjust scores based on issuer-specific insights, including the credibility and execution of climate transition strategies. This granular, bottom-up approach allows us to identify climate-related risks and opportunities at the issuer level and reflect them in our valuation and risk compensation models.

9. Describe the climate-related risks and opportunities you have identified over the short, medium, and long term.

Although material/key climate-related risks vary from industry to industry, the team expects transition risks to be something that will most likely have more impact in the short to mid-term. Physical risks related to climate change on the other hand are more likely to have greater impact in the medium to long term, as the frequency and intensity of climate change related disasters is more likely to increase.

In the Canadian landscape, the key sector that the team has identified to be exposed to transition risk is the energy space. In recent years, the team has regularly passed on new issues of Integrated Oil & Gas companies (esp. long bonds), as the team is becoming increasingly concerned about stranded asset risks with traditional oil companies. While the companies are presently generating very strong cash flows, the energy transition poses significant challenges and requires these companies to make substantial investments in technology to meet emission reduction targets and other environmental standards. Also, with increasing electrification of mobility, there is growing risk of oil losing its relevance as the main energy source. Since we only invest in companies that have outlined a clear path towards emission reduction going forward and in strong actors in this space, we are mostly avoiding long dated maturities of these issuers (e.g. >15yrs) as uncertainty around stranded assets etc. will challenge the business model over time.

Regarding physical risks, the team is still looking to get a better sense of assessing how these will impact specific sectors (e.g. insurance sector where we already observe increasing claims as a result of changing weather patterns). The IFI team is aware of the development of tools within Fiera to better capture the potential impact on portfolio returns; however, these still need to be refined. When the team believes there could be a material impact on the business or financial profile of an issuer due physical risk concerns, it is factored into the assessment of the issuer’s securities and the team modifies their judgement on the required returns to compensate for the additional risk factors.

10. Describe how you analyze the effectiveness of your investment strategy when taking into consideration different climate-related scenarios, including 1.5 degree and 2 degree Celsius warming scenarios.

When assessing the resilience of the investment strategy, the team currently relies on credit analysis factoring in their own proprietary research, but also extensively leverages MSCI ESG research and data. Using the MSCI data as a starting point, the team has created a proprietary ESG scoring system that completes the coverage out of scope from MSCI and also adjusts scores across the E, S and G pillars where the team has come to a different conclusion and reflective of their views. This proprietary Fiera ESG Score equips the team with the necessary data to more effectively compare the ESG profile and carbon metrics across issuers to better identify outliers and establish points of potential engagement with company management. Additionally, it helps the team to identify companies that require a higher degree of compensation for their assessed risk relative to peers.

The investment strategy is resilient and allows for consistent outperformance across market environments as a result of the investment process's dynamic approach which aims to exploit diversified sources of alpha. Top-down factors, including duration, yield curve, and sector positioning, allow the team to define their strategy and establish a quantitative framework. Bottom-up factors focus on credit research reviews which helps portfolio managers identify attractive securities. Environmental, Social and Governance (ESG) factors, including climate change related risks are accounted for in the fundamental analysis of a company because they have the potential to affect company value in the long run. Additionally, our ESG data provider provides us with different carbon metrics that are used in our own carbon monitoring and carbon attribution reports. The investment team has been increasingly incorporating carbon data into company analysis and leverages the data to work towards its goal to effectively quantify the carbon footprint of its portfolios in relation to their respective benchmarks.

While the team does not explicitly consider the 1.5 degree and 2 degree Celsius warming scenarios in its credit research, the portfolios are constructed to have a meaningfully lower carbon intensity than their respective benchmarks – coupling the lower average emissions and higher average ESG score with the strong performance track record gives the team confidence in the effectiveness of the investment strategy.

11. Do you track the carbon footprint of portfolio holdings?

Yes – we track the carbon footprint of our portfolio holdings. We also generate and provide Climate Risk Reports (that contain carbon footprint metrics) and Carbon Metrics and Attribution Reports for our different portfolios and benchmarks.

If yes, how frequently? Please provide the results as of December 31, 2023 and describe the methodology and metrics used, including whether you have set targets and/or a net zero objective for reducing the portfolio’s footprint, and comment on any related progress over the past year.

Through MSCI ESG research, we have access to carbon emissions data and other climate-related data points that enable us to generate Climate Risk Reports and Carbon Metrics and Attribution Reports described above. These reports provide financed emissions and carbon intensity emissions information on Scopes 1,2 and 3 basis.

Our proprietary ESG scoring also allows customization to achieve client objectives. This may include Fossil Fuel Free portfolios that excludes debt from energy companies, as well as issuers in nonenergy sectors with high carbon intensity, strategies focused on excluding issuers with a high risk of loss from current or past controversies and carbon intensity focused portfolios that seek to reduce the portfolio’s carbon footprint over time or relative to a benchmark.

12. What are your firm's emissions? Please demonstrate how/whether you are taking steps to reduce these emissions.

Similar to our investment portfolios, we are equally committed to minimizing our operational carbon footprint. In 2025, we partnered with Planet Mark to assist us in calculating our corporate GHG emissions across all our locations and we have since been awarded with their Planet Mark Business Certification. The Planet Mark certification is a recognized symbol of sustainability progress that verifies and measures carbon data, supporting efforts to cut emissions and contribute to the achievement of the SDGs.

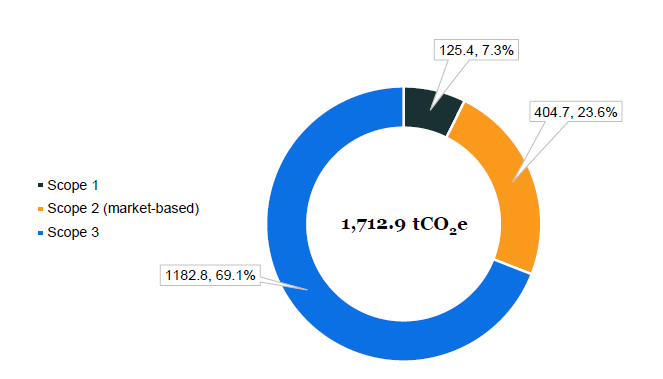

Summary of our operational emissions (we are awaiting more up-to-date results as of the time of this questionnaire)

Reporting year:

January 1, 2023, to December 31, 2023 1

Reporting boundary:

Fiera Capital (Global Operations)

Highlights (market-based2):

Measured carbon footprint (tCO2e): 1,712.9 tCO₂e

Measured carbon footprint per employee (tCO2e): 2.0 tCO₂e

Measured emissions:

Scope 1: Diesel Fuel, Natural Gas

Scope 2: Electricity

Scope 3:

Cat. 1: Purchased Goods & Services (partial measurement)

Cat. 3: Fuel & Energy-Related Activities (partial measurement)

Cat. 5: Waste

Cat. 6: Business Travel

Cat. 7: Employee Commuting (partial measurement)

Measured Carbon Emissions by Scope for year 2023, tCO2e 3:

1.Most recent data available

2.Market based method: A market-based method reflects emissions from electricity that companies have purposefully chosen (or their lack of choice).

3.Source: Planet Mark, Data as of December 31, 2023.

Furthermore, Fiera Capital attempts to conduct its operations in a carbon-neutral manner by reducing the carbon footprint of our operations as much as possible. Various grassroot-level initiatives are underway or being considered to improve the footprint, such as those related to employee travel.

To minimize the depletion of natural resources and to reduce waste and greenhouse gas emissions, Fiera Capital applies sound environmental practices to all operations. Depending on the office, these practices include but are not limited to:

- Improved sorting for recycling/garbage

- Eliminating single use products: straws, cups, water bottles

- Battery & electronic waste recycling

- Limiting energy usage by installing motion sensors on the floor and in offices, and using energy efficient lightbulbs

- Replacing bottled water with pitchers for onsite meetings

- Considering more sustainable, local caterers that use either reusable plates/cutlery or compostable containers

- Incorporating sustainable considerations for office supplies that limit waste and are more earth-friendly (less plastic)

Additionally, our office building in Toronto has a BOMA Go Green Plus Certification and holds RCO The Recycling Council of Ontario – Green Team, among other awards.

13. For the mandate you manage for Queen’s, what percentage of equity holdings (if applicable) have credible net zero commitments?

Not applicable for fixed income investments.

14. How do you assess the credibility of a company’s emission reduction targets?

The team believes that engagement can improve issuer performance and reduce an issuer’s risk profile while better aligning behaviour with client interests. Ahead of each engagement, we set clear objectives for what we want to achieve – this can vary across issuers depending on their ESG risk exposure, sector or history. At a high level, the objectives typically revolve around:

- Establish or understand emission reduction targets and if they have been publicly disclosed

- Transparency around target setting/intentions

- Data and disclosure around specific ESG factors, in particular carbon emissions and intensity with expected improvement in accuracy and inclusion of Scope 3 over time

- Request further data and verify currently published data to make sure we can accurately compare companies within the sector and adequately assess emission elated risks

Our objective is to understand clearly the company’s intentions, strategy and targets, and ensure we have proper data and disclosure to track progress to hold management accountable.

15. What forward-looking metrics do you use to assess an investment’s alignment with global temperature goals?

The credit team focuses on engagement as their most effective tool to translate portfolio decarbonization to economy decarbonization. The Canadian energy sector produces significant GHG emissions and faces heightened levels of scrutiny from investors and other stakeholders. There is a real risk that energy companies will face funding challenges in the future if they do not address this issue and do not sufficiently disclose data on their emissions and set clear emission reduction targets.

A key objective of the team has been to clearly understand how energy companies within our coverage will get to their 2050 Net Zero target, including what resources are they putting in place, what investments are they planning to make, and what interim targets have they established to assess progress, among others. The team needs to ensure that issuers take these issues seriously and are not simply making loose commitments.

Overall, we believe engagement is the most effective tool to translate portfolio decarbonization to economy decarbonization. We are not interested in companies simply selling off their dirty assets to other actors, which in effect reduces emissions of the selling issuers so they appear greener but does not improve emissions overall. Rather, we encourage issuers towards the decommissioning of “brown” assets (where possible) to be replaced by green technology. We believe that remaining engaged, laying out expectations, and giving companies time to execute on their transition strategy, while still holding companies accountable in the interim is an effective strategy to address climate related risks and align with global temperature goals.

As an outcome of our continued partnership with MSCI ESG, we now have access to advanced climate metrics and data points including those on energy transition readiness, Implied Temperature Rise and Climate Value at Risk (CVaR). We will look to familiarize ourselves with these metrics and assess the potential for incorporating these into our investment decision making processes.

16. Has your firm produced a Task Force on Climate-Related Financial Disclosures (TCFD) report? If yes, please provide a link to the most recent report.

Yes, we have published TCFD-aligned reports over the past few years. Our 2024 Climate Report is aligned with the recommendations of TCFD and available on our website.

Going forward, we intend to fully integrate our climate disclosures into our comprehensive Sustainability Report. We feel this integrated approach is consistent with market developments, in particular the move towards a global baseline of sustainability disclosure and the transferring of climate-related disclosure responsibilities from the TCFD to the IFRS Foundation. Our climate-related disclosures will continue to be consistent with the four core recommendations and 11 recommended disclosures of the TCFD.

17. Has your firm produced a Sustainability Accounting Standards Board (SASB) report? If yes, please provide a link to the most recent report.

No.

However, we are a SASB supporter and our Sustainability/Climate Reports have been informed by the Asset Management & Custody Activities industry standard.

Diversity

18. Please provide the composition of your senior leadership team and board of directors, including women and visible minorities. How do you encourage diversity of perspectives and experience?

Fiera Capital has an established Diversity, Equity and Inclusion (DE&I) governance structure empowered to advance best practices and support meaningful progress across the organization.

Fiera Capital believes that embracing diversity of thought and lived experience strengthens decision-making, fosters innovation, and enhances our ability to serve clients globally. Creating a respectful, inclusive, and supportive culture remains central to our long-term business strategy and sustainability.

DE&I Governance and Leadership

DE&I efforts at Fiera are led by HR and supported through a dedicated internal governance model. Building on the strong foundation established through our Global DE&I Council and Ambassador Network, Fiera has evolved its approach to ensure sharper focus, stronger accountability, and sustainable execution over time.

Today, DE&I priorities are guided through an agile Steering Group and embedded across key functions including Talent Acquisition, Employee Engagement, Learning & Development, and ESG.

Strategic Focus Areas

Fiera’s DE&I strategy is structured around key pillars designed to promote inclusion across the employee lifecycle and strengthen representation:

- Inclusive Workforce – advancing diverse representation and equitable access to opportunities

- Inclusive Workplace – fostering belonging, psychological safety, and inclusive leadership practices

- Inclusive Partnerships – building external partnerships that support the communities we serve

Key Initiatives and Accomplishments (Past Three Years)

Over the past three years, Fiera has implemented several impactful initiatives, including:

- Launch of a more inclusive and competitive Global Parental Leave Policy. Organization-wide training programs on Unconscious Bias, Respect at Work, and Allyship for all employees. Ongoing participation in leadership development programs such as The A Effect’s Ambition & Leadership Challenge, supported through the Women at Fiera Community.

- Achievement and maintenance of the Bronze Level Parity Certification from Women in Governance in the US and Canada since 2022

- Launch of an Indigenous Engagement and Inclusion Pledge (2024), reinforcing our commitment to meaningful partnerships.

- Development of active Employee Resource Groups supporting Women, BIPOC, LGBTQ+, Mental Health, and Working Parents.

- Introduction of a firm-wide Volunteering Program, offering employees one paid day annually to support community engagement. Implementation of a Global Recruitment Policy to promote consistency, fairness and diverse talent pipelines. Strategic partnerships with organizations such as the Ivey Business School’s WAM (Women in Asset Management) Program.

- Early adoption as one of the first signatories of the CFA Institute Diversity, Equity, and Inclusion Code for the Investment Profession in the United States and Canada.

- Fiera Capital received the Diversity, Equity and Inclusion award at the Institutional Connect Awards in 2024, that recognizes the outstanding and authentic commitment of the firm in its inclusion efforts, within the organization and with external partners.

Board Members Gender representation:

Male: 70%

Female: 30%

Board Members Ethnicity representation:

Not disclosed

Senior Leadership Gender representation:

Male: 94%

Female: 6%

Senior Leadership Ethnicity representation:

White: 75.0%

Asian: 6.25%

Declined to answer: 18,5%

Proxy Voting

19. Do you use an external proxy voting service such as ISS or Glass Lewis? If yes, please specify.

Yes - Institutional Shareholder Services Inc (“ISS”).

20. If the answer to the previous question is no, please describe your proxy voting guidelines.

Not applicable.

21. If you use an external proxy voting service, do you customize your guidelines for proxy voting? If yes, describe your customized guidelines. If you use the default service guidelines, describe how often and in which situations you deviate from the external proxy voting service recommendations.

Fiera Capital and its portfolio managers do not delegate the proxy voting responsibility to a service provider. However, we hire the services of an external proxy advisory service provider to generate research as well as customized voting recommendations based on Fiera Capital’s guidelines. The service provider helps manage the proxy voting process in collaboration with the sustainable investing team and each investment management team’s dedicated individuals who oversee share voting.

The current service provider we use is Institutional Shareholder Services Inc. (“ISS”), an independent firm with expertise in global proxy voting and corporate governance issues, to manage proxy voting activities.

In 2025, 92% of our votes were aligned with our service provider’s recommendations. While our service provider’s research is an input in the analysis of the proxies we vote for, our voting decisions are taken independently from their recommendations.

22. What proportion of the time do you vote with or against management on shareholder resolutions, board appointments, and auditor appointments? What proportion of the time do you vote with or against management on ESG issues? How does this break down for climate, diversity, and remuneration issues?

Please find attached to this questionnaire Fiera Capital’s 2025 proxy voting statistics.

Engagement

23. What are your engagement goals? Are these goals outcome/action-based (e.g. decreases in emissions or increases in number of women on the board) or means-based (reporting on emissions or number of women on the board)?

Our engagement priorities focus on issues that are material to issuer credit quality, ESG risk management, long-term value creation, and the need to maintain a well-informed view of issuer fundamentals. We routinely engage with issuers during funding discussions and management meetings to clarify business strategy, assess financial strength, and validate risk factors.

With respect to ESG specifically, our priorities focus on the issues most material to issuer credit quality and long-term resilience, including improved disclosure and data quality, governance practices, and credible environmental transition planning. Environmental factors (particularly emissions transparency and transition readiness), governance oversight, and select social issues make up the majority of our ESG-related engagements. These priorities reflect where engagement can meaningfully reduce risk, improve issuer behaviour, and support long-term value creation for clients.

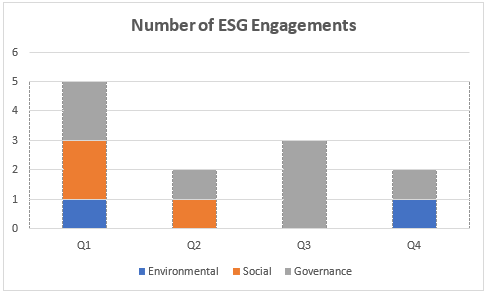

Breakdown by Area of Engagement

Number of Management Meetings: 69

Number of ESG Engagements: 12

Breakdown by Area of Engagement:

• Environmental: 2

• Social: 3

• Governance: 7

24. What is your policy around the escalation of engagement; how and why might this happen and what is the ultimate tool you might use (e.g. voting against board re-election, etc.)?

As the team is actively participating in funding discussions with corporate issuers on an ongoing basis, the team’s exposure to management teams is significant and the nature of the discussions gives the team the right levers for engagement. Should an engagement not deliver the right outcome and/or the team will conclude that they are not adequately compensated for ESG specific risks related to the issuer, the team would typically pass on the new issue and/or provide specific feedback to the issuer (either directly or through the dealers). Additionally, in some cases where they already have substantial exposure to an issuer, the team might decide to exit a bond position. Since they are fixed income investors, voting against board re-election etc. are tools that are typically not available to them.

25. Describe a specific example of your firm’s engagement with a company over the past year, including the outcome and any lessons learned.

Over the past year, we engaged with a large Canadian utilities company – the objective was to deepen our understanding of the issuer’s climate strategy, including the pace of planned sustainability upgrades and its approach to managing environmental risks across its asset base. Management provided updated detail on their operational plans, evolving net-zero alignment considerations, and the expected trajectory of Scope 2 emissions. This allowed us to clarify assumptions within our credit and ESG analysis and to monitor how their plans were maturing.

For us, this constitutes a successful engagement, not because it produced a binary pass/fail outcome, but because it strengthened transparency, enhanced our insight into the issuer’s forward-looking transition profile, and positioned us to track tangible progress over subsequent quarters. IFI’s engagement framework is designed around ongoing, iterative discussions that improve the quality of information, help validate or challenge issuer narrative.