ESG Policies

1. Please provide your ESG-related policies. Please provide a formal statement of your ESG-related policies if you have one.

Yes. We are guided by our values to do the right thing for our environment, society and each other. Our purpose is simple: investing for a better tomorrow. We believe that delivering the best investment outcomes for our clients over the long term depends on securing a prosperous and sustainable future.

To achieve this, we place sustainability at the core of our business, via our three-dimensional sustainability framework: Invest, Advocate, Inhabit.

ESG policies

There are two policies that govern the ESG space at Ninety One.

• Sustainability policy

• Stewardship policy and Proxy Voting guidelines

Our policies have evolved over time, however our original policy (then called the 'Stewardship policy') was put in place when we constituted the Sustainability Committee in 2009.

Ninety One's Sustainability Policy addresses Ninety One’s approach to sustainability. It covers the full sustainability framework at Ninety One, which comprises three pillars: Invest, Advocate and Inhabit.

We look to ensure high-quality ESG integration processes and frameworks across all of our investment strategies. These include equity, fixed income, multi-asset and alternative strategies. Our commitment to incorporate ESG issues into investment analysis is ‘investment-led’, which means that each of our investment teams integrates and prioritises ESG issues in line with its investment philosophies and processes, while ensuring compliance with the policy. Our aim is to ensure that robust integration processes highlight material sustainability risks and opportunities, spanning environment, social and governance, and prompt our investment teams to analyse and address them as part of their fundamental research. Our approach is based on the belief that, over time, the market will increasingly price externalities into the value of securities, and that investment outcomes can be improved by a deep understanding of material ESG-related risks and opportunities and their potential to affect value.

The policy applies to all Ninety One entities and all investment products across asset classes. While the principles and approach described apply to all assets in which Ninety One invests, the policy may be applied differently according to the environment in which the company operates. Ninety One recognises that governance and corporate culture differ worldwide, and takes these differences into account in its engagements with boards and company management teams.

The policy should be read in conjunction with our ‘Stewardship policy and proxy voting guidelines’, which detail our approach to encouraging broader long-term shareholder value through our engagements and proxy voting.

2. Are sustainable investing and ESG factors integrated into your investment process and portfolio management decisions? If yes, please provide details.

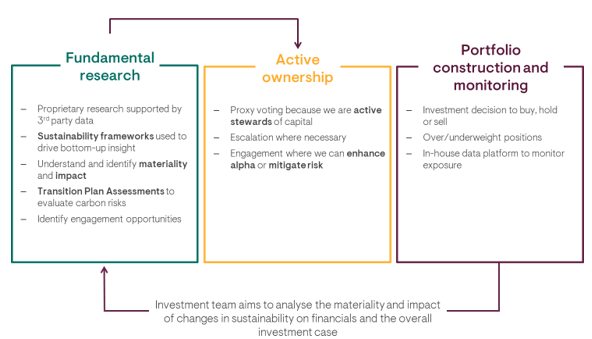

We integrate sustainability into our fundamental analysis and decision making to unlock the alpha potential these opportunities may represent or mitigate risks on the downside. Below we set out how sustainability is integrated in our process.

Alpha model

We have recently incorporated ESG features into our alpha model, selected based on potential impact, data type, coverage, and materiality. Early analysis indicates that, while ESG features provide useful additional insight, traditional financial metrics have historically shown a stronger correlation with alpha generation. As such, ESG inputs have not yet made a material contribution to model performance, though we continue to monitor their impact closely. Importantly, ESG considerations remain fully integrated into our fundamental analysis, where they play a key role in identifying material opportunities and risks that can either enhance alpha potential or mitigate downside, whether financial or reputational.

Fundamental research

Materiality matrix

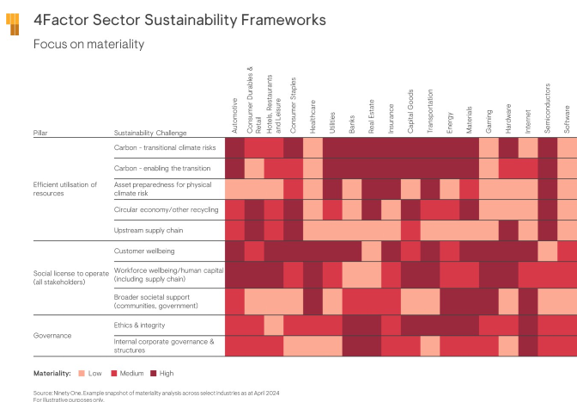

To systematically analyse ESG information, we prioritise materiality and impact for both opportunities and risks. Our ESG assessments leverage a materiality matrix through three-pillars across ten key sustainability challenges, ranked high, medium or low, depending on the level of perceived risk.

This process is guided by a bottom-up sector sustainability framework informed by our team’s specialist sector knowledge. Recognising the breadth and specificity of challenges and opportunities inherent to each sector, we tailor our approach to ensure relevance. For example, carbon is an obvious challenge for sectors like materials and energy, but it’s far less of an issue for, say, healthcare. In healthcare, we are far more concerned about ethics and integrity.

We have found that insights generated from our materiality matrix help us to identify areas where financial returns could be under threat or improved and we utilise these within our fundamental research. The framework also provides a basis for guiding the investment team on engagements on the most material sustainability challenges for companies in each sector, to help catalyse a positive alpha outcome or otherwise mitigate risk, be it financial or reputational.

The ESG considerations considered most material in our investment process vary by sector but broadly include environmental issues such as carbon emissions and climate transition risks, social factors like ethics, labor conditions, and customer safety, and governance elements such as board oversight and executive compensation. ESG analysis is an ongoing part of our fundamental research and due diligence on both potential and current investments.

Transition Plan Assessment

When committing to net zero as a firm, we were conscious that most companies globally, but particularly in emerging markets, did not yet have a clear plan on how they are going to decarbonise by 2050. Therefore, we were keen to ensure, in our role as shareholders, we could encourage, engage and measure the high emitters in our portfolios on the progress of their transition to Net Zero. Where possible, we want to go on the journey of transition alongside the heavy emitting companies that we hold across our firm. Given the bias of these companies towards emerging markets, this is particularly relevant for this mandate.

To ensure that we do this with integrity, we have developed an in-house, firm wide, ‘Transition Plan Assessment’ (TPA) that scores our heaviest emitters on three key principles: level of ambition, credibility of plan, and implementation of plan. This is used to assess heavy emitting companies within the portfolio. It helps to inform and prioritise our company engagements with those where climate is likely to be a material risk, as well as deepening our understanding of their business and its vulnerability to a disorderly transition.

We undertake TPAs for all securities that, once invested, contribute to the top 50% of firm-wide financed emissions.

Engagement

As active stewards of our client's capital, we believe it is not only our duty to engage with companies, but that these engagements can form a critical input in our fundamental research.

Our engagement strategy targets specific holdings and material ESG themes that are significant to the firm, the investment team, and our clients. We do not engage with every company in our portfolio. We are also realistic with how much influence we can have, as this can be dependent on our shareholding in the company. Therefore, the trigger to engage with a company is if we believe that our involvement will mitigate a material risk (financial or reputational) and/or catalyse an alpha-positive outcome. Our approach to engagement therefore prioritises companies that have experienced a development that could potentially materially impact their intrinsic value or proactive engagement where we believe we can add to shareholder value. For instance, the work undertaken through our TPAs combined with the deep, subjective understanding of our investment analysts, can help us to pre-empt potential issues through engagement. We document dialogue with companies, and monitor and report on engagements, measuring success and outcomes against initial objectives, such as commitment to, or enactment of, actual changes by management in strategy or reporting, disclosure and transparency. We also report on goal progress to our clients.

Portfolio construction

In part, portfolio size is determined by a sustainability analysis. Ultimately, we will not own a company where there are material sustainability risks, and any increase in such risks will trigger a reassessment of our entire investment position in the company. We monitor risk, including ESG risks, within the portfolio across various dimensions. No bottom-up process can effectively operate in a vacuum: we consider these externalities in-line with other non-stock specific risk factors to be material potential drivers of risk and return in the portfolio, particularly over longer-term time horizons.

ESG Risk monitoring

It is worth noting that while our portfolio managers have ultimate responsibility for monitoring and maintaining an optimum risk/reward balance in their portfolios, including ESG risks, further guidance and support is provided by the Ninety One Investment Risk team (including dedicated ESG specialists), which oversees and challenges the investment process.

Ninety One’s ESG risk framework seeks to monitor, assess and challenge on ESG risks in investment portfolios, including reputational risks. The purpose of the ESG risk process is to ensure ESG integration is in place within investment processes and strengthen existing integration efforts by testing its robustness through appropriate challenge. Note that the aim is not to expunge ESG risk from Ninety One portfolios, rather to ensure it is identified and understood, and that relevant exposures are justified and risks mitigated in terms of overall client and stakeholder outcomes. ESG risk reporting forms part of the monthly Investment Risk Committee (IRC), which oversees the governance of all aspects of investment risk. ESG risk reporting also forms part of the reporting to the Sustainability Committee which oversees the overall response by the business to its commitment to ESG integration, including the effectiveness of the risk component.

3.a. Are you a signatory to the UNPRI?

Yes.

3.b. If you are signatory to other coalitions, please list them.

As a global business, we welcome the development of stewardship codes across the world. We believe that these codes are key to enhancing the long-term success of companies, through a better quality of engagement and improved transparency in regional markets. We are currently an endorser/signatory to the following codes:

• UK Stewardship Code

• Code for Responsible Investment in South Africa (CRISA II)

• Singapore Stewardship Principles

• Hong Kong Principles for Responsible Ownership

• Japan's Stewardship Code

• Korea Stewardship Code

3.c. Indicate any other international standards, industry guidelines, reporting frameworks, or initiatives that guide your responsible investing practices.

We seek to contribute meaningfully to the conversation on sustainability and to encourage a deeper focus on sustainability-related issues in all of the jurisdictions where we invest, always to the benefit of our clients and their long-term investment outcomes. We may collaborate with other investors as part of an engagement strategy if it can contribute to achieving our engagement objectives and can help address the relevant risks. Our membership of regional and global organisations facilitates this.

The table below details our firmwide collaborative partnerships and our role:

| Organization | Start date |

Key focus | Our role |

|---|---|---|---|

| Abu Dhabi Sustainable Finance Declaration | 2023 | Participate in regional industry initiatives signalling commitment to sustainable finance. | We are signatories and join monthly meetings on progress on Sustainable Finance in Abu Dhabi, and participate in local events hosted by ADSFD or ADGM where relevant. |

| Access to Medicine Foundation | 2023 | Expand access to medicine and encourages healthcare companies to do more to reach people in low- and middle-income countries. | Ninety One has pledged support to the Foundation’s research and signed the Access to Medicine Index Investor Statement. |

| Assessing Sovereign Climate related Opportunities and Risks (“ASCOR”) project |

2021 | Develop a globally adopted climate assessment framework for sovereigns’ performance and governance on climate – including a just transition. | We are advisory board members and funders of Phase 2 of the ASCOR project. |

| Association for Savings and Investment South Africa (ASISA) |

2008 | Ensure that the South African savings and investment industry remains relevant and sustainable into the future in the interest of its members, the country and its citizens. | We actively participate in collaborative engagements and working groups and serve on the Responsible Investment Committee. Thabo Khojane, Managing Director of our South African business, is a member of ASISA's board and several committees, including the Executive Committee. |

| Chatham House Asia-Pacific Programme |

2018 | Provide objective analysis of issues affecting APAC, engage decision-makers and undertake research to inform and influence policy. | We aim to actively contribute to conversations with academics, diplomats and policymakers. |

| CDP | 2010 | Advocate for and implement increased disclosure on climate, water and forest for increased transparency. | We participated in the no-disclosure campaign. Two investee companies we have engaged with disclosed to CDP on Climate Change in 2024. |

| TheCityUK Green and Sustainable Finance Group | 2026 | Focus on ensuring UK policy and regulations promote the UK as an internationally competitive and globally attractive destination for green investment. | We are a working group member. |

| Climate Action 100+ | 2018 | Ensure the largest corporate emitters take climate action. | We are involved in collaborative engagements with companies to ensure they minimise and disclose climate risks. We co-lead on three companies. |

| Crisis Group | 2014 | Works to shape policies that will build a more peaceful world. | We leverage Crisis Group’s expertise in our investment decision-making and engagements. We are involved with its Ambassador Council and are members of its Peacebuilding Society. |

| Emerging Markets and Developing Economies (EMDE) Investor Taskforce | 2025 | To unlock private investment aimed at tackling climate change and seizing sustainable growth opportunities across emerging markets and developing economies. | Our CEO is an industry co-chair of the Taskforce. |

| Emerging Markets Investor Alliance |

2019 | Enable institutional EM investors to support good governance, promote sustainable development, and improve investment performance. | We are involved in working groups, particularly relating to fiscal transparency, leading on some and participating in others. |

| Farm Animal Investment Risk and Return) FAIRR |

2019 | To raise awareness of the material ESG risks and opportunities caused by intensive livestock production | We participate in collaborative conversations to identify and engage on material ESG risks and opportunities in protein supply chains. |

| The Food Foundation | 2025 | Driving change in food policy and business practice to ensure everyone can afford and access healthy and sustainable food. | We participate in meetings and conversations to gain further knowledge on food policy and business practice to ensure everyone in the UK can afford and access a healthy diet. |

| Glasgow Financial Alliance for Net Zero (GFANZ) |

2021 | Convene firms from leading net zero initiatives across finance to accelerate the transition to net zero by 2050. | We are members of the Principal and Steering Group for GFANZ. We are on the GFANZ Africa Board and actively participate in other ways. |

| Global Climate Finance Centre (GCFC) |

2023 | Drive the transformation of the UAE’s financial markets and institutions towards a more sustainable future. | We participate as Steering Committee members in the strategic direction of the GCFC and contribute to collateral, expert discussions and other deliverables. |

| Global Investor Commission on Mining 2030 |

2023 | Recognise the mining industry’s role in the energy transition, and the need for it to manage systemic risks. | We are members of the Steering Committee. We reviewed the Landscape Report, launched in October 2024. |

| ISSB Investor Advisory Group | 2025 | Improve the quality and comparability of sustainability-related financial disclosures. | Our CSO is a group member. |

| Institute of International Finance (IIF) |

2021 | Support the finance industry to manage risks, develop best practices and advocate for policies that foster stability and sustainable growth. | We participate in global membership meetings and collaborative efforts on global financial policy and regulatory matters. |

| Institutional Investors Group on Climate Change (IIGCC) |

2018 | Provide investors with a collaborative platform to encourage policies, practices and behaviour that address climate risks and opportunities. | We co-chair the investor practices programme and participate in the net zero implementation and corporate bond stewardship working groups. |

| The Investment Association (UK) |

2002 | Help the finance industry support the economy, provide access to fair and effective markets, and embed standards of sustainable governance. | We are full members and take part in various working groups. |

| The Investor and Issuer Forum | 2025 | Enhance the effectiveness of UK equity markets with a clear focus on sustainable value creation. | Hendrik du Toit is on the Steering Committee. |

| The Investor Forum | 2017 | Position stewardship at the heart of investment decision-making. | We participate in targeted strategic governance engagements. |

| Investor Leadership Network |

2022 | Create a collaborative platform for addressing sustainability and long-term growth. | We contribute to three workstreams: private capital mobilisation, diversity equity and inclusion and climate change. We contributed to the Blended Finance Handbook. |

| National Business Initiative |

2022 | Work towards sustainable growth and development in South Africa and shape a sustainable future through responsible business action. | We contribute to the working groups focused on South Africa’s net-zero transition and transition finance. We sponsored the NBI South African pavilion at COP29. |

| Nature Action 100 | 2023 | Drive greater corporate ambition and action to reverse nature and biodiversity loss. | We have joined four collaborative engagements to improve nature-related disclosures at focus companies. |

| Net Zero Asset Managers Initiative (NZAMI) |

2021 | Support investing aligned with net zero by 2050. | We are a signatory and have set net zero targets. We have submitted our targets to the initiative and report progress annually. |

| PRI | 2008 | Understand the implications of ESG factors and support investor signatories in incorporating them. | We are a signatory, participate in workstreams, present at UNPRI events and take part in collaborative engagements. |

| Responsible Investment Association (RIA) Canada |

2021 | Promote responsible investment in retail and institutional markets | We aim to support the RIA to advance responsible investment in Canada. |

| SOAS China Institute | 2021 | Promote research and teaching on China, channelling expertise to government and business. | We aim to actively contribute to conversations with academics, diplomats and policymakers. |

| Sustainable Markets Initiative (SMI) |

2021 | Accelerate the transition to a sustainable future by engaging public, private and philanthropic sectors. | We participate in the Asset Manager/ Asset Owner Taskforce and Blended Finance Taskforce. |

| Task Force on Climate-related Financial Disclosures (TCFD) |

2018 | Develop consistent climate-related financial risk disclosures for companies, banks and investors. | We support the recommendations and publish a TCFD report in our Integrated Annual Report. |

| Task Force on Nature-related Financial Disclosures (TNFD) Forum |

2022 | Develop a risk management and disclosure framework for nature-related risks. | We aim to support consultative work to develop the TNFD recommendations, including via the TNFD forum. |

| Transition Finance Council | 2025 | Raise and deploy transition finance in the UK. | We are members of working groups on ‘credibility and integrity’ and ‘scaling transition finance’. |

| Transition Pathway Initiative (TPI) |

2019 | Assess companies’ preparedness for the energy transition. | We support the initiative and use the data it produces to assist our understanding of climate risks and opportunities. |

| World Bank Private Sector Investment Lab | 2023 | Develop solutions that address existing barriers to private sector investment in emerging markets and developing economies. | We are members of working groups developing solutions that increase catalytic equity and risk-mitigation instruments. |

4. Please describe how ESG oversight and integration responsibilities are structured at your firm, including the process for escalation of key ESG issues. Also, if applicable, describe how responsible investment objectives are incorporated into individual or team employee performance reviews and compensation mechanisms.

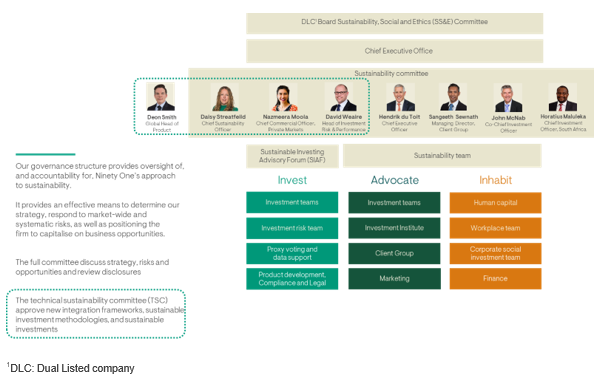

The following chart provides an overview of the governance of our sustainability approach across Invest, Advocate and Inhabit:

Our Sustainability team is the central custodian of the firm-wide sustainability framework and ecosystem. They report into the Sustainability Committee which is responsible for the internal oversight of sustainability, including monitoring progress and ensuring alignment of focus, strategy and integrity through the business. The Sustainability Committee reports to the Chief Executive Office, which in turn reports to the Ninety One Board and the Sustainability, Social and Ethics Committee (SS&E).

A detailed description of each of the functions mentioned above and how they assist with ESG integration and analysis across the firm is given in the following table:

| Roles | Function |

| Sustainability, Social and Ethics Committee | The Board has ultimate responsibility for ensuring that the business is managed in the best interests of its stakeholders, which include our shareholders, our clients, our people, the communities we operate in, and the natural environment. Sustainability is one of Ninety One’s five strategic priorities.

Ninety One’s Board considers the contribution of Ninety One to sustainable development, including addressing climate change, a priority. A key element of this is overseeing and reviewing risks and opportunities that may have a material impact on Ninety One. |

| Chief Executive Office |

Ninety One’s executive management team is responsible for developing and implementing business strategy, under the direction of the Chief Executive Officer (CEO). This will include assessing Ninety One’s exposure to sustainability risks. These risks in our portfolios are overseen by the Chief Investment Officer (CIO) office alongside Ninety One’s investment risk infrastructure. |

| Chief Sustainability Officer | Ninety One's Chief Sustainability Officer (CSO) is responsible for overseeing our firmwide sustainability initiatives. This includes investment integration, advocacy, corporate transition to net zero and developing and implementing efforts to mobilise dedicated funding for an inclusive net zero transition.

The CSO reports directly to the CEO and Co-CIOs signalling the importance of the invest dimension to sustainability. |

| Sustainability Committee | The Sustainability Committee was established in 2010 and is responsible for the internal oversight of sustainability, including monitoring progress and ensuring alignment of focus, strategy and integrity through the business.

Ultimately, the committee endeavours to drive a cohesive response to our sustainability priorities, set by the executive leadership by Ninety One. The Committee is chaired by the Chief Sustainability Officer and is comprised of senior leaders representing core areas of the business, including Ninety One’s CEO, Head of Investment Risk & Performance, Chief-Investment Officers and Managing Director of Client Group. They meet quarterly to review progress and activities in relation to strategy, risks and opportunities, and to review disclosures. The Sustainability Committee delegates to the Technical Sustainability Committee (TSC) the authority to manage specific technical and operational sustainability matters on its behalf. These include new integration frameworks, sustainable methodologies, sustainable product updates and regulatory/disclosure compliance. Deon Smith, Global Head of Product, joins the TSC to contribute to technical sustainability product-related discussions. |

| Sustainability team | The Sustainability team sets the overall sustainability strategy, including our firm-wide net-zero targets and our advocacy priorities; aligns teams on strategic engagements; and provides specialist knowledge and guidance on issues like transition-plan assessments, just transition, governance frameworks, engagement approaches and voting. |

| Sustainable Investment Advisory Forum | The Sustainable Investment Advisory Forum (SIAF) is the internal review and guidance forum for issues in relation to sustainable investment and Ninety One’s Sustainable Strategies and Sustainable Mandates. These are the Ninety One funds and mandates that fall in to the sustainability classification framework by Ninety One (sustainable or impact) and would correspond to either a category 8 or category 9 as per the EU sustainable finance regulations. The forum is chaired by Nazmeera Moola, Chief Sustainability Officer, and is typically attended by members of the Sustainability team and the portfolio managers for the sustainability strategies.

The forum bears the responsibility for reviewing and guiding the organisation around the sustainability standards for new and existing portfolios. It has no formal powers but plays a critical role in its advice and guidance to other formal groups and committees including the SRB, the Sustainability Committee and Global Product Committee. The forum and its members serve as a central point of excellence and insight when it comes to sustainability strategies and what constitutes a sustainable investment. |

| Investment teams | Ninety One’s investment teams have ultimate responsibility for managing sustainability risks and opportunities, through their own integration frameworks.

Each of our investment capabilities uses a distinctive investment process that reflects its investment philosophy. Heads of each of the investment capabilities at Ninety One are ultimately responsible for driving the ESG agenda within their strategies and portfolios. They frequently attend and report into the Sustainability committee. Portfolio managers as well as analysts are responsible for ESG considerations in respect of their Strategies. This means building a holistic understanding of the ESG risks in each of their positions and how to price these risks. Then through strategic engagements identify areas that we can improve or mitigate these risks over time. In addition, informal ESG champions are embedded in investment teams. |

| Investment Risk | The Investment Risk team includes a dedicated ESG Risk function that monitors firm and portfolio-level sustainability risks. They perform a ‘safety net’ function to identify, and challenge objectively on, ESG issues.

The ESG risk-monitoring framework assumes that ESG risks are identified, analysed and acted upon by investment teams. The purpose of the ESG-risk process is to ensure this integration is a systematic part of the investment process and to strengthen existing integration efforts by testing their robustness through dialogue and challenge. The Investment Risk team test the robustness of the ESG integration within investment processes with an internal ESG risk-monitoring framework. At the firm level, they monitor exposure to investments that flag on various third-party ESG metrics. |

| Proxy Voting specialists and data support | Within operations, a dedicated team administers proxy voting. Within IT, a team supports the investment teams by integrating and surfacing ESG data. |

| Investment Institute | Ninety One’s Investment Institute is an engagement platform that delivers strategic investing insights and analysis to our clients across asset classes, investment strategies and borders.

They provide in-depth analysis and research on key geopolitical, economic and investment trends. Their work draws on our firm’s investment capabilities and partnerships with leading academics and external practitioners and seeks to empower our clients with insight and knowledge. With this collaboration, central themes of the Investment Institute’s work have been portfolio resilience, sustainability and the application of ESG principles to investing. These have culminated in the publication of annual journals and papers. They seek to play a full and active role in the global conversation on sustainable investing. From aligning a portfolio with the decarbonisation growth trend to ensuring a fair clean energy transition for all, Ninety One’s portfolio managers and analysts explore sustainable investing across asset classes and investment approaches. |

| Client group | Client groups help to lead the sustainability conversation. They look to help provide thought-provoking content, training, events and partnerships, with the aim to help our clients tackle the issues that are impacting their investments. |

| Human Capital team | The Human Capital team help to ensure we are looking after our people.

They look to help create a culture where we can collectively achieve together, as teams, without losing the sense of individual identity. They cover topics such as workforce engagement, organisational and talent development, diversity and inclusion, wellbeing, equality and health & safety. |

| Workplace teams | The workplace team look to ensure that we are running our business responsibly and acting sustainability within our operations. They oversee our corporate sustainability strategy across five focus areas: energy, waste, water, sustainable travel and responsible procurement — with the aim of reducing and mitigating our carbon footprint. |

| Corporate Social Investment team | The CSI team is responsible for our corporate social investment strategy which spans three pillars: conservation, education and community development. |

5. How do you obtain ESG information/data (e.g. public information, third party research, reports and statements from the company, direct engagement with the company)? Please provide specific details of what information is obtained from each source, and how this information is acquired.

Our sustainability team and investment risk team look to ensure that the business has appropriate access to ESG data, so that investment teams are equipped with the knowledge, research and tools to fully integrate ESG into their investment processes. The data that we have access to is used to support understanding of material information. We use a combination of proprietary and external research, which is integrated and considered in various ways depending on the investment team process for example through scorecards, through use of investment data platforms, and use in research reports.

The table below summarises the primary ESG data sources that we make use of:

| Provider | Product | How we use the research and data |

|---|---|---|

| MSCI ESG | Company ESG research providing characteristic view of the business, rating, controversy flag, and thematic data such as carbon data | We make use of the data in different ways including analysis of company reports and ratings, as well as consideration of raw data |

| CDP (formerly Carbon Disclosure Project) | Carbon emissions data and qualitative assessment of company activities | We use the data to assess and understand exposure to climate change related risks, and analysts may use company disclosures on the CDP platform |

| ISS ProxyExchange | Voting recommendations and governance research around company Annual General Meetings | We make use of ISS research to inform our voting decision |

| RepRisk | Monitoring platform for negative ESG news flow | RepRisk reports are distributed to analysts on request, and RepRisk data is made available to analysts, highlighting news flow contributing to reputational risk |

| Bloomberg | Bloomberg collects, verifies and continually updates ESG data from published company disclosures | We use various Bloomberg ESG data points to support our integration work |

| Clarity AI | Tech-based reporting tool to ensure compliance with relevant regulatory frameworks | We leverage the data to assist us with assessing and complying with our regulatory obligations i.e. SFDR requirements |

| In-house investment data platform (Jasmine) | Our proprietary investment data platform aggregates data from several sources to give investment teams direct access to a range of portfolio management metrics, which include ESG metrics for individual securities and portfolios alongside financial data. | We use the platform for:

• Surfacing specific data points i.e. carbon data, MSCI data o ESG data distribution for portfolios |

6. What channels do you use to communicate ESG-related information to clients and/or the public? Do you produce thought leadership (written reports and publications)? If so, is the information available to the public? Please provide links, if applicable.

Transparent reporting and communication with clients and stakeholders are key features of our “sustainability with substance” approach. We believe that being transparent about our stewardship approach is important, and this is reflected in our reporting to clients. We publish several regular and bespoke reports, which include:

Sustainability and Stewardship report

The Sustainability and Stewardship Report outlines how the firm integrates sustainability into investing, advocates for positive systemic change, and reduces its own environmental footprint to help build a more sustainable future, including integration highlights, engagement details, advocacy work, voting data, case studies and market trends. The report is published annually covering the previous year to 31 March.

PRI Transparency and Assessment reports

As a signatory, we report on our responsible investment practices through the PRI Transparency report. Our latest PRI reports can be found on our website via the following link: https://ninetyone.com/-/media/documents/stewardship/91-pri-public-transparency-report-en.pdf

Task Force on Climate-related and Nature-related Financial Disclosures (TCFD and TNFD)

Ninety One formally pledged its support for the TCFD in September 2018 and this report sets out how we disclose our exposure to and management of climate risk, using the TCFD framework. In 2025, we also incorporated our disclosures to to the TNFD. Our TCFD and TNFD report can be found within our Integrated Annual Report (pages 38-51)

Online voting disclosure

Voting decisions are disclosed publicly on a monthly basis on the Ninety One website and can be found our website via the following link: https://ninetyone.com/en/united-states/sustainability/invest-advocate-inhabit/invest/proxy-voting-results.

Annual Sustainability Reports

With regard to our sustainability-focused products, our annual sustainability reports present significant developments throughout the year, including environmental and sustainability metrics for the portfolios and underlying holdings, details on proxy voting (where applicable), as well as engagement goals and progress:

- Global Environment Impact Report

- Global Sustainable Equity Sustainability Report

- Emerging Markets Sustainable Blended Debt Sustainability Report

Quarterly Sustainability Reports

For several of our our non sustainability-focused products, our Quarterly Sustainability Reports provide an outline of the key sustainability risks and opportunities and cover the investment team's approach to sustainability integration; key engagements; proxy voting activity; portfolio climate risk analysis and portfolio characteristics.

Other sustainability disclosures

We publish various sustainability disclosures on our website as per regulatory requirements i.e. SFDR disclosures.

Investment Institute

Our Investment Institute is an engagement platform that delivers strategic investing insights and analysis to our clients across asset classes, investment strategies and borders.

The Investment Institute provides in-depth analysis and research on key geopolitical, economic and investment trends. Its work draws on our firm’s investment capabilities and partnerships with leading academics and external practitioners, and seeks to empower clients with insight and knowledge.

Portfolio resilience, sustainability, and ESG applied to investing have been central themes of the Institute’s work and have culminated in the publication of annual journals and papers. Below are just a few of our research, reporting and thought leadership papers relating to Sustainability that we have produced. All are both, internal and public-facing communications.

The Investment Institute mobilizes Ninety One’s firm-wide expertise and our substantial global network of specialist partners to generate proprietary insights on the global economy, markets, geopolitics and asset allocation. The Institute seeks to play a full and active role in the global conversation on sustainable investing. From aligning a portfolio with the decarbonization growth trend to ensuring a fair clean-energy transition for all, Ninety One’s portfolio managers and analysts explore sustainable investing across asset classes and investment approaches.

An important feature of our Investment Institute is the direct link between the research insights it generates, and portfolios managed across the firm. The Institute works closely with all the firm’s investment capabilities and has strong Executive Management support for its work.

Podcasts

Through our ‘The Big Picture’ podcast channel we provide interviews and viewpoints on various ESG related topics.

7. Do you have periodic reviews of your ESG process/approach to assess its effectiveness? If so, how frequent are the reviews? What are the results? What would cause you to disregard ESG issues in your investment/analysis decisions?

At Ninety One, responsibility for evaluating ESG risks and opportunities lies first and foremost with the investment team managing the strategy. Within the 4Factor team, ESG analysis is conducted by the same analysts who perform fundamental financial analysis, ensuring it is fully integrated into the investment case and intrinsically linked to our research process. Portfolio managers have ultimate accountability for investment decisions and portfolio construction, including the assessment and management of ESG risks and opportunities.

This structure embeds ESG accountability throughout the investment process. Analysts and portfolio managers are expected to build a holistic understanding of the material ESG risks and opportunities associated with each holding. Their views are challenged through constructive debate within the team and subject to oversight from the Sustainability

and Investment Risk teams. ESG integration and stewardship are also reinforced through firmwide governance structures, including the Sustainability Committee, chaired by our Chief Sustainability Officer, and the Sustainable Investment Advisory Forum.

To support this integration, the investment team is complemented by Ninety One’s central Sustainability team and the dedicated ESG Risk function within the Investment Risk team. The Sustainability team provides firmwide frameworks, tools, training and best practice guidance, as well as leading strategic initiatives such as our proprietary TPA framework for high-emitting companies. The Investment Risk team performs an independent “safety net” role, monitoring portfolios on ESG risks at both company and portfolio levels, providing high level challenge on integration quality and risk mitigation effort.

Importantly, ESG integration forms part of our investment professionals’ performance assessments, directly linking responsible investment practices to remuneration. This ensures that ESG considerations are not treated as a separate function but are embedded into decision-making, accountability, and incentives across the investment team.

Data gaps and inconsistencies are a well-recognised challenge in emerging markets, which is why we do not rely exclusively on third-party ESG ratings. While we use data providers such as MSCI ESG and RepRisk to provide inputs and controversy monitoring, these are treated as reference points rather than investment signals.

Our approach is fundamental and investment led, with analysts validating information directly through company engagement and by drawing on multiple alternative sources, including suppliers, customers, competitors, industry consultants, and site visits where possible. This allows us to test company disclosures, highlight inconsistencies, and develop a deeper understanding of how ESG risks and opportunities might play out in practice.

Because our analysts follow companies in depth and over long periods, they can form forward-looking views that go beyond reported data, assessing not only current sustainability practices but also the credibility of management strategies and capital allocation. This is particularly important in emerging markets, where disclosure is often backward looking and incomplete.

We see this as a key benefit of anchoring our investment framework in fundamental analysis, led by our sector and regional specialists. ESG integration is most effective during this stage, where analysts can apply judgement, test disclosures, and bring forward looking insight into company research. The depth of our fundamental work allows us to go beyond reported metrics, capturing the nuance of management behaviour, strategy and governance. In doing so, our analysts can identify material ESG risks and opportunities, whether financial or reputational, that may not be fully reflected in third-party data.

By blending these perspectives, we can address data gaps more effectively and ensure ESG considerations are integrated where they are most material to the investment case and to long-term risk-adjusted returns.

Climate

8. Describe how you identify, assess, and manage climate-related risks, and whether climate-related risks and opportunities are integrated into pre-investment analysis.

As an active global investment manager, we approach climate change with a dual focus on transition and physical risks, ensuring alignment with the interests of all our stakeholders, including our staff, clients, shareholders, and the companies in which we invest. The greatest risk to our business lies in the potential material destruction of value in the companies to which we allocate our clients’ capital. For this reason, the deep integration of climate change risk within our investment process is essential for safeguarding long-term business resilience.

We integrate climate change considerations into our investment decision-making process, prioritising both transition and physical risks where material. This involves assessing climate change risk exposure at both the investment and portfolio levels, actively engaging with investee companies on climate-related issues, and supporting industry initiatives to improve the quality and availability of climate-related disclosures.

To enhance our capabilities, we have developed tools to measure portfolio carbon metrics aligned with the Taskforce for Climate-related Financial Disclosures (TCFD) recommendations and the Partnership for Carbon Accounting Financials (PCAF) standard. Building on the development of our proprietary Portfolio Climate Risk Tool, which provided critical insights into methodologies and data challenges.

Within the 4Factor investment process, we conduct analyses of carbon emissions and transition pathways for all prospective investments. Carbon transition is a material risk for many sectors, necessitating a dual approach at both stock and portfolio levels. We are also expanding beyond carbon risk profile analysis to emphasise transition alignment and the quality of companies’ transition plans. This evolution is supported by ongoing training for investment professionals, such as the bespoke climate risk program conducted with Imperial College, which has fostered organisation-wide debate and informed the development of transition alignment frameworks at the strategy level. Our dedicated Sustainability team continues to guide investment teams and support engagement with clients on their net-zero agendas.

Our approach to addressing climate change is rooted in materiality, focusing on the companies responsible for 65% of Scope 1, 2, and 3 emissions, as outlined by the UN Net Zero Asset Owners Alliance. For high-emitting companies, we employ the 4Factor-specific Transition Plan Assessment, a comprehensive framework that evaluates emissions intensity, science-based reduction targets, TCFD reporting alignment, net-zero ambitions, transition pathways, and the alignment of management incentives with these goals. Companies are categorised into five transition alignment tiers—“Achieving Net Zero,” “Aligned,” “Aligning,” “Committed,” or “Not Aligned”—based on criteria from the Institutional Investors Group on Climate Change (IIGCC) energy transition framework.

9. Describe the climate-related risks and opportunities you have identified over the short, medium, and long term.

We systematically assess both transition and physical climate-related risks and opportunities through our bottom-up sector sustainability framework and our proprietary TPAs, in line with Nest’s requirement that managers evaluate both forms of climate risk.

Specifically, one of the three pillars of our sector sustainability framework is "Efficiency Utilisation of Resources" which is then further broken down into five challenges, including (i) carbon - transitional climate risk, (ii) carbon - enabling the transition, and (iii) asset preparedness for physical climate risk. Through evaluation of these challenges, we identify and more deeply understand the materiality and impact posed by climate-related risk. We apply a proprietary materiality matrix within the framework to systematically assess which sustainability challenges are most relevant for each sector. The matrix ranks issues as high, medium or low materiality, ensuring that climate-related risks such as carbon emissions, physical preparedness, and transition planning are evaluated consistently and with financial materiality in mind.

In addition to this, our TPAs enable our investment team to evaluate and measure the ambition, credibility and implementation of a company’s transition plan. The assessment and understanding of such risks, where they exist, then puts us in a position to engage with a company where appropriate.

Insights from TPAs and the sector sustainability framework can shape our engagement approach to catalyse an alpha-positive outcome, or to mitigate material risk (either financial or reputational), helping to inform stock selection and portfolio construction decisions, with the objective of influencing real-world carbon reduction.

We evaluate the materiality of ESG issues that could pose a risk to the value creation in the underlying companies most integrally in our fundamental analysis, where sustainability risks and opportunities of a portfolio company are assessed holistically across time horizons. For instance, governance issues may be more short-term and hence, should we identify issues in this space, they would form a key part of our materiality analysis as well as our engagement and voting decisions. Bribery scandals, accounting irregularities, or weak board oversight are examples of uses which could directly impact a company's financial performance and stock price in the short term. On the other hand, the focus around climate change and other structural changes within an industry will bring out more long-term ESG issues. Climate change considerations, including both transition and physical risks where material, are considered in a natural order in our fundamental analysis and decision-making process.

10. Describe how you analyze the effectiveness of your investment strategy when taking into consideration different climate-related scenarios, including 1.5 degree and 2 degree Celsius warming scenarios.

Ninety One performs climate scenario analysis to better understand our firmwide exposure to, and management of, climate risk consistent with the Taskforce for Climate-Related Disclosures (TCFD) framework and recommended disclosures. We do not systematically incorporate climate-scenario analysis in the investment decision making process for this strategy. However, we are able to do so to support clients' assessments of their portfolios where requested.

Our preferred approach to climate risk analysis is to consider climate risk implications and opportunities on investment valuations using available data and fundamental research. This includes considerations such as carbon prices and forecasts, policy mechanisms such carbon tax, and data from companies that gives us a real sense of the economic cost, including from physical risks to corporate assets. Currently, we believe much of this information is best understood through fundamental research and engagement. Reducing complex long term trajectories within different scenarios to a single metric such as VAR may be misleading given the extent of estimation and assumptions in the underlying data.

To date much of the firm’s focus towards managing these risks and uncertainties has been on forward looking qualitative work and understanding transition plans starting with the highest emitting investments across our asset base. As part of the Emerging Markets Equity strategy, a Transition Plan Assessment is carried out for all stocks that, once invested, contribute to the top 50% of firm-wide financed emissions.

While climate-scenario analysis can enable us to gain a deeper understanding of the physical and transition risks in our portfolios, we remain cautious about its accuracy, given the multitude of variables involved in climate modelling and the very long modelling timeframes. Nevertheless, we see it as a useful addition to our bottom-up analysis of company-specific risk.

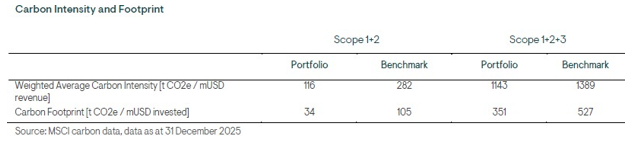

11. Do you track the carbon footprint of portfolio holdings? 11a) If yes, how frequently? Please provide the results as of December 31, 2025 and describe the methodology and metrics used, including whether you have set targets and/or a net zero objective for reducing the portfolio’s footprint, and comment on any related progress over the

past year.

Yes. The analysis below is based on all assessable securities held directly within the portfolio as at the end of the quarter as estimated using the methodology described above. For the purposes of this analysis, where only a percentage of the portfolio is covered as at 30 September 2025, the assessable securities have been reweighted to 100%. This only affects the carbon intensity measure. Therefore, the carbon intensity reflects only the emissions of companies where we have data and may not be reflective of the emissions of the entire portfolio. This quarter we’ve changed the Carbon Footprint measure to align with observed changes in the industry. Using the Partnership for Carbon Accounting Financials (PCAF) guidance, we now use Enterprise Value including Cash (EVIC) to determine the allocation of emissions.

Scope 1 & 2 emissions provide a good proxy for how efficiently a company is managing the carbon emissions directly under its control. Data for Scopes 1 & 2 has decent coverage and is relatively consistent quarter on quarter reflecting portfolio and benchmark changes. However, for many sectors, like oil & gas or automotive companies, Scope 3 accounts for the bulk of emissions. This includes the carbon emissions in both the company’s supply chain and those generated by the company’s products as they are used. Therefore, we also provide Scope 3 data, when this accounts for the most significant portion of a company’s emissions. We would caution that the quality of Scope 3 data is less advanced, it is not reported by all companies and where it is, it may not be calculated on a consistent basis. We use estimates based on sector averages where it is not available or incomplete and are regularly refining the modelling underpinning Ninety One’s climate-risk tool to improve accuracy. This leads to greater variability in the Scope 1, 2 & 3 columns for both the portfolio and benchmark. This means that it is difficult to compare Scope 3 emissions quarter-to-quarter. However, as we aim to have an impact on real world emissions, we believe that engagement priorities can only be set including Scope 3 emissions.

Carbon reduction targets

We do not manage the Strategy to explicit climate related targets. However, Ninety One's net zero targets currently incorporate our entire portfolio of corporate assets. These targets aim for 56% of AUM and 50% of financed emissions have science based targets and net zero transition plans by 2030 and are applied across the firm's overall portfolio of investments, as opposed to individual strategies. Therefore, the corporates held in this portfolio are part of the scope of these overall targets. We also engage with companies guided by areas identified in their TPAs to influence real-world carbon reduction.

In our drive for low-emitting portfolios, we intend to do more than reduce ‘portfolio carbon’ by simply constructing portfolios that exclude high-emitting companies. If we mechanistically apply an exclusionary process to achieve net zero targets, a consequence is likely to be the creation of portfolios concentrated in asset-light industries without the transition focus on the remainder. As a side-line, we might see certain companies, regions and sectors abandoned to their own devices.

12. What are your firm's emissions as of December 31, 2023? Please provide scope 1 and scope 2 emissions, and, separately, scope 3 emissions if available. Please demonstrate how/whether you are taking steps to reduce these emissions.

Our commitment to sustainability extends beyond integrating it into the way we invest. The third pillar of our sustainability framework 'inhabit', drives our ambition to inhabit our own ecosystem in a manner that ensures a sustainable future for all. This includes the way in which we look after our people and the way we govern our firm. As a long-term investor on behalf of our clients, we are aware of our broader responsibility to society.

Change starts with us, and we are committed to walking our talk in terms of our own sustainability footprint. We enthusiastically take on the responsibility for ‘inhabiting’ our ecosystem in a manner that ensures a sustainable future for all. From the Ninety One Green Team at our offices, through to our work in conservation and communities both globally and in our original homeland of Africa, we support the preservation of our natural world, creating a better tomorrow for future generations.

Running our business responsibly

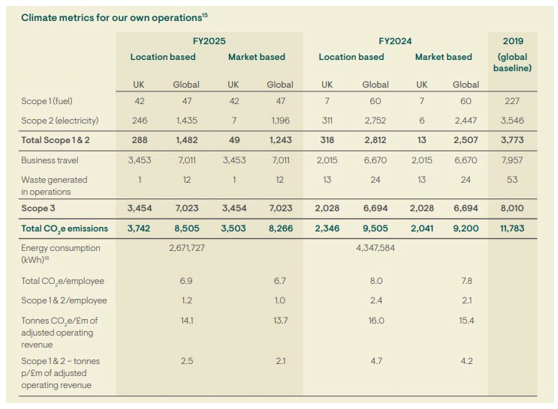

Ninety One joined the Net Zero Asset Managers Initiative in 2021, committing to reach net zero emissions by 2050 or sooner. We published our transition plan in 2022, which includes 2030 targets for our investments and operations.

As an investment manager, the largest contribution to our carbon footprint is from the investments that we make on behalf of our clients. At the same time, in line with our purpose, we want to contribute to a better world, and aim to run our business sustainably. We are committed to reducing emissions across our own operations and locations and have set a 2030 target to reduce absolute Scope 1&2 emissions by 46%. As at 31 March 2025, we had reduced absolute Scope 1 and 2 emissions (location based) by 61% vs. our baseline of 2019. This was primarily due to a temporary reduction in office space at our interim Cape Town location. This is expected to normalise once we return to our refurbished office, albeit at a lower level than historical emissions given the focus on sustainability during the refurbishment project. Our target is a reduction of 46% by 2030.

We are committed to reducing our direct operational impact and improving the sustainability of our offices globally. Over the past year, we refined our environmental data-collection processes to enhance the accuracy and completeness of our reporting. This included improving carbon-emissions tracking, refining data quality and adjusting historical estimates.

15. Emissions metrics are calculated to align with Ninety One’s financial year, with the exception of 2019, which was calculated for a calendar year. The update was applied in FY2022 following recommended sustainability accounting standards.

16. Energy consumption in kWh for Scope 1 and Scope 2. Global includes UK GHG emissions.

We measure and report our carbon emissions following the Greenhouse Gas (“GHG”) Protocol’s Corporate Accounting and Reporting Standard (revised edition). This allows us to track progress against our carbon-reduction targets transparently. We measure and report our carbon using both location- and market-based methodologies. We believe this provides the most transparent and accurate view of our operational carbon footprint.

Key carbon numbers

- Total tCO₂e per £million of adjusted operating revenue, our intensity metric, decreased by 12% in FY2025 due to the reduction in electricity emissions noted below. This reflects ongoing efforts in operational efficiency and emissions management.

- Scope 2 electricity emissions decreased by 48% on a location basis. This was primarily due to a temporary reduction in office space at our interim Cape Town location. This is expected to normalise once we return to our refurbished office, albeit at a lower level than historical emissions given the focus on sustainability during the refurbishment project.

- Scope 3 emissions, which include business travel, waste, and paper use, increased by 5% to 7,023 tCO₂e in FY2025. We maintain our commitment to mitigating these emissions through carbon credits and other initiatives.

- Scope 1 & 2 emissions decreased by 47% in FY2025. Compared to our 2019 baseline, these emissions have decreased by 61%, keeping us on track to achieve our 2030 reduction target.

Decarbonising our operations

While our direct emissions are small compared to the broader investment industry, we believe in leading by example. We continue to:

- Partner with BioCarbon Partners (“BCP”): Our collaboration with BCP offsets 100% of our Scope 1, 2 and business travel-related Scope 3 emissions. This initiative supports forest conservation and community engagement in Zambia’s Luangwa and Lower Zambezi regions.

- Improve office sustainability: Our Cape Town office refurbishment integrates sustainability at its core, contributing to significant energy savings and a reduced carbon footprint.

- Engage employees in sustainability: Through our Ninety One Green resource group, we encourage employees to take action on sustainability. This year, our campaigns focused on explaining COP29 and raising awareness about how fashion and clothing contribute to our individual carbon footprints.

We remain focused on continuously improving our environmental performance. While sourcing renewable energy in some locations remains challenging, we are exploring viable options to increase clean-energy use across our offices.

13. For the mandate you manage for Queen’s, what percentage of equity holdings (if applicable) have credible net zero commitments? Please answer on both an equally-weighted and market cap-weighted basis.

We do broadly aim to build portfolios which exhibit lower WACI than the benchmark. However, we also recognize there is more to this topic than current emissions metrics. A critical part of our fundamental investment process it to understand the direction of travel; by assessing the credibility of our target companies’ own commitments and proposed transition pathways.

As a percentage of NAV 2.4% of the portfolio consists of companies with SBTi commitments, while on an equally weighted basis, this figure is 2.5%. These are commitments demonstrate an organizations’ intention to develop targets and submit these for validation within 24 months. This would be the first step in setting a science-based target.

As a percentage of NAV, 19.2% of the portfolio consists of companies with validated SBTi targets, while on an equally weighted basis, this figure is 19.0%. These companies have clearly defined pathways to reduce greenhouse gas (GHG) emissions, which have been validated by the SBTi.

14. How do you assess the credibility of a company’s emission reduction targets?

As mentioned above, at a firm level, we have developed a process to assess the transition risk of the biggest emitting companies in our house portfolio. When committing to net zero, we were conscious that most companies globally, but particularly in emerging markets, do not yet have a clear plan on how they’re going to decarbonize by 2050. Therefore, it is our role as shareholders to encourage, measure and engage the high emitters in our portfolios on their transition and to go on the journey of transition alongside them, with a special focus on emerging markets. To ensure that we do this with integrity, we have developed an in-house ‘Transition Plan Assessment’ (TPA) that scores our heaviest emitters on three key principles: level of ambition, credibility of plan, and implementation of plan.

Our current 4Factor investment process includes comprehensive analysis of the carbon emissions and transition pathways of our prospective investments that are material to the net zero transition. Carbon transition is highlighted as a material risk for many sectors, necessitating both a stock and portfolio-level approach. We are now working on ways to expand from our portfolio carbon risk profile analysis to place greater emphasis on transition alignment and the quality of companies’ transition plans.

The 4Factor specific Transition Plan Assessment for high portfolio emitters provides a holistic assessment looking at emissions intensity, reduction targets if these are science based, TCFD reporting alignment, net zero ambitions, transition pathways, and alignment of management incentive structure linked to achievement of goals. We categorize these high emitters into five categories, to align with the IIGCC energy transition criteria: “Achieving Net Zero”, “Aligned”, “Aligning”, “Committed” or “Not aligned” as appropriate.

15. What forward-looking metrics do you use to assess an investment’s alignment with global temperature goals?

As an organisation, we believe in transition alignment, and in SBTi as the gold standard for companies to comply with. As a signatory to NZAMI, we are committed to setting out a plan to reach net zero by 2050 or sooner. We are committed to ensuring that 100% of our corporate asset pool (debt and equity) achieves Net Zero by 2050.

At a firm level, we have sought to design net-zero targets for our investment teams aimed at driving real-world carbon reduction and allowing emerging markets to transition in a fair and inclusive manner. To this end, we have set the following target for our investments:

- At least 50% of the corporate emissions financed by Ninety One will be generated by companies with Paris-aligned science-based transition pathways by 2030.

- The proportion of our corporate assets under management covered by Paris-aligned science-based transition pathways will meet the SBTi requirements for Ninety One to obtain a verified SBTi. We calculate this requirement to be 56% of our corporate assets under management with science-based transition pathways by 2030.

- In practice, we will be engaging actively with our highest emitters and largest holdings to maximise the proportion of our corporate AUM with science-based transition pathways.

Whilst the portfolio has no explicit net zero target, we should note that the transition alignment evaluation, enables us to monitor the portfolio from a climate risk analysis perspective, and allows us to actively engage with the companies that are top emitters in the portfolio.

We would expect more of the portfolio through time to be aligned to a net zero pathway.

16. Has your firm produced a Task Force on Climate-Related Financial Disclosures (TCFD) report? If yes, please provide a link to the most recent report.

Yes, Ninety One formally pledged its support for the Task Force on Climate-related Financial Disclosures (TCFD) in September 2018, reinforcing our commitment to climate change.

Our TCFD reporting sits within our Integrated Annual Report (pages 38-53). Our TCFD report provides a summary view of how Ninety One is supporting each of the disclosure recommendations applicable to investment managers. Please refer to the recommendations table from page 39, which outlines our progress on each of the TCFD recommendations. The table shows both areas in which we have made good progress and areas where we believe more work is required to fulfil a disclosure requirement to a high standard.

As per FCA requirements, we have also included additional metrics where required for the assets in scope of the FCA’s UK entity level requirements, which include the AUM of Ninety One Fund Managers Limited and investments managed by Ninety One UK Limited.

To meet FCA product level requirements, we also report TCFD metrics for our UK domiciled OEIC fund range and have also begun providing specific information on scenario analysis which can be found for each OEIC fund here. Ninety One has based its analysis of the impact of climate risk on the three TCFD scenarios for greenhouse gas (GHG) emissions pathways and the inferred carbon prices developed by the Network for Greening of the Financial System (“NGFS”) – an orderly transition scenario, a disorderly transition scenario and a hothouse-world scenario.

17. Has your firm produced a Sustainability Accounting Standards Board (SASB) report? If yes, please provide a link to the most recent report.

Not applicable

Diversity

18. Please provide the composition of your senior leadership team and board of directors, including women and visible minorities. How do you encourage diversity of perspectives and experience?

Across the firm, we have a diverse, experienced and stable leadership team.

Board of Ninety One Ltd and Ninety One plc

The Board of Ninety One Ltd and Ninety One plc (“the Board”) is responsible for, inter alia, the approval and review of the Ninety One Ltd and Ninety One plc group of companies’ (“Ninety One Group”) long term objectives and strategy, approving any dividend payments, ensuring maintenance of a sound system of internal control and risk management and oversight of financial position, investment performance and operations.

The Boards consist of six Non-Executive Directors and two Executive Directors.

Executive Management

The Board, with Executive Management, agree the strategy for the business and ensure the right structures are in place to achieve success. Executive Management regularly reviews and monitors progress against Ninety One’s strategic objectives. Where factors arise which may impede (or accelerate) the execution of these priorities, they are carefully considered and appropriate action is taken. The Board is kept abreast of progress on Ninety One’s strategy, including material developments which may arise, so they may opine on new developments, including risks.

In terms of key operating decisions, different topics are discussed at meetings per set agendas.

The Executive Management at Ninety One consists of key senior managers and our original founders. The Executive Management represents continuity and stable leadership:

Our Executive Management are supported in their roles by highly skilled and experienced business unit heads that have direct responsibility for activity in their individual markets. Our depth of talent provides us with highly competent and experienced professionals who could take the reins in the event of a leadership change. We have successfully transitioned in times of change – maintaining or even enhancing investment and operational performance and this is testament to the robustness of our structure.

Diversity and inclusion

'Doing the right thing' is part of our cultural identity and underpins everything we do at Ninety One. We recognise that inclusive workplaces, where individuals from all backgrounds can contribute fully, drive better business outcomes. Fostering a fair and respectful environment is also a reflection of our core value of doing the right thing—for our clients, shareholders, colleagues, and the communities in which we operate.

At the core of our values is the respect for the dignity and worth of the individual. We are committed to attracting and retaining exceptional talent by offering an inclusive and merit-based environment where individuals from all backgrounds can grow and thrive professionally. While there may be minor nuances between the laws of the different countries in which we operate, the concepts outlined in our Equality Policy enshrine our global approach to the principles of equality, embracing diversity and doing the right thing.

This policy respects the dignity and worth of the individual and aims to attract and retain the best talent by providing a corporate environment where people from varying backgrounds can develop professionally and build a rewarding career.

We summarise our philosophy to diversity and belonging under 5 pillars:

- Diversity Commitment:

- As an active asset manager, we build diverse teams to create better outcomes for our clients

- Cultural Alignment:

- Our core values of ‘doing the right thing’ and ‘freedom to create’ shape our approach to inclusion and belonging, reinforcing our ability to innovate and perform.

- Freedom to Thrive:

- We operate within a meritocratic framework and recognise that individuals may face different starting points. We aim to provide equitable access to opportunity so all employees can realise their potential.

- Shared Accountability:

- We hold ourselves and our leaders accountable for creating a diverse and inclusive workplace

- Belonging and Inclusion:

- We cultivate an environment where people feel they belong, enabling engagement and better outcomes

Proxy Voting

19. Do you use an external proxy voting service such as ISS or Glass Lewis? If yes, please specify.

Yes. We use an external proxy research and vote execution service provided by Institutional Shareholder Services (ISS) to produce tailored reports. ISS provide us with a service through which they deliver both their benchmark research and Ninety One’s custom policy research. Ninety One does not outsource the voting decision, as we carry out the decision and execution of the vote in-house using the online voting platform provided by ISS.

These reports include vote recommendations (not instructions) that arise from applying Ninety One’s voting guidelines. The vote decision is then reached by the relevant investment teams in accordance with the investment philosophy, supported by an operational Voting team. Through this rigorous voting process, we can be certain the voting done is in the best interest of our clients.

20. If the answer to the previous question is no, please describe your proxy voting guidelines.

Not applicable

21. If you use an external proxy voting service, do you customize your guidelines for proxy voting? If yes, describe your customized guidelines. If you use the default service guidelines, describe how often and in which situations you deviate from the external proxy voting service recommendations.

Ninety One treats proxy voting as an integral part of its overall engagement strategy. The firm uses proxy voting not only to exercise its ownership rights but also as a tool to drive meaningful change when dialogue with company management has not yielded sufficient results. Proxy voting is embedded in a broader stewardship framework that begins with thorough fundamental analysis—including an assessment of ESG risks—and is followed by active engagement with company leadership.

When significant issues arise, Ninety One’s investment and sustainability teams work together to decide on a vote, guided by clearly defined proxy voting guidelines. These guidelines focus on key areas such as leadership quality, long-term strategic alignment, managing sustainability risks (including climate change), protecting client capital, and ensuring transparent audit and disclosure practices. The voting process is carried out in-house, with decisions informed by external proxy research reports, and executed electronically. Furthermore, the firm publicly discloses its voting decisions and the rationale behind any negative votes, reinforcing accountability and transparency.

This approach ensures that proxy voting acts as a direct extension of Ninety One’s engagement efforts, helping to safeguard client assets while promoting better corporate governance and sustainable business practices

22. What proportion of the time do you vote with or against management on shareholder resolutions, board appointments, and auditor appointments? What proportion of the time do you vote with or against management on ESG issues? How does this break down for climate, diversity, and remuneration issues?

Ninety One Proxy Voting Summary

| Firm wide | |||

| Vote type | For | Against | Abstain |

| Board appointments | 45.1% | 1.8% | 1.0% |

| Strategic Transactions | 2.1% | 0.2% | 0.0% |

| Other | 1.3% | 0.1% | 0.0% |

| Routine Business | 10.6% | 0.2% | 0.0% |

| Capitalisation | 9.6% | 1.0% | 0.0% |

| Company Articles | 2.5% | 0.2% | 0.0% |

| Mutual Funds | 0.0% | 0.0% | 0.0% |

| Compensation | 13.1% | 0.8% | 0.1% |

| Auditor appointments | 6.2% | 0.1% | 0.0% |

| Diversity | 0.0% | 0.2% | 0.0% |

| Shareholder resolutions | 0.8% | 1.1% | 0.1% |

| Takeover Related | 0.8% | 0.0% | 0.0% |

| Social | 0.4% | 0.0% | 0.0% |

| E&S Blended | 0.1% | 0.0% | 0.0% |

| Climate | 0.1% | 0.0% | 0.0% |

| Non-Routine Business | 0.1% | 0.0% | 0.0% |

| Procedural/Non-Equity | 0.0% | 0.0% | 0.0% |

| Emerging markets equity fund | |||

| Vote type | For | Against | Abstain |

| Auditor appointments | 4.28% | 0.42% | 0.14% |

| Board appointments | 33.52% | 3.09% | 1.96% |

| Capitalisation | 8.06% | 0.98% | 0.00% |

| Company Articles | 6.17% | 0.77% | 0.35% |

| Compensation | 11.22% | 0.56% | 0.07% |

| Other | 6.31% | 0.49% | 0.07% |

| Routine Business | 16.55% | 0.14% | 0.35% |

| Shareholder resolutions | 1.05% | 0.42% | 0.28% |

| Social | 0.35% | 0.14% | 0.00% |

| Strategic Transactions | 1.96% | 0.21% | 0.00% |

| Takeover Related | 0.00% | 0.07% | 0.00% |

Engagement

23. What are your engagement goals? Are these goals outcome/action-based (e.g. decreases in emissions or increases in number of women on the board) or means-based (reporting on emissions or number of women on the board)?

Active ownership is a vital component of Ninety One’s investment management process. Our investment teams use their influence as active stewards of our clients’ capital to engage with companies and other entities on sustainability issues including direct and systemic risks. Exercising ownership rights, including engagement and proxy voting, is a means through which we can enhance the value of client assets and deliver on the expectations of our clients. Our Stewardship policy and proxy voting guidelines document explains our voting and engagement approach.

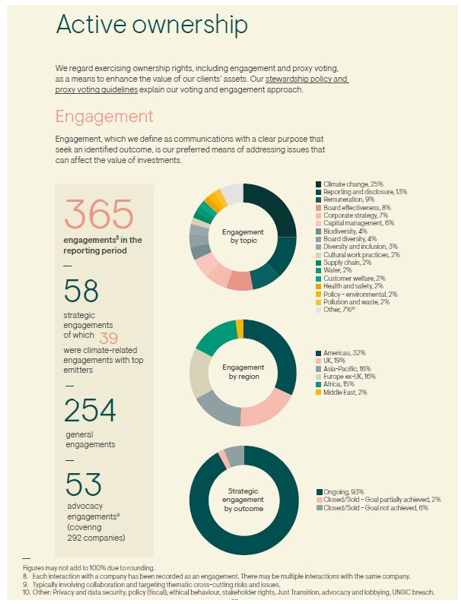

Ninety One sees engagement as the preferred means to address material risks and issues that can affect the value of the investments we make on behalf of our clients. Engagements are communications with a clear purpose that seek an identifiable outcome. To identify a need for engagement, Ninety One will assess the materiality of the issue, the potential impact of engagement, both positive and negative, and its ability to exert influence.

Ninety One has two engagement categories:

Strategic

Firmwide priority engagements to address critical, systemic, or market-wide risks and opportunities.

General

Entity specific engagements carried out by capabilities as part of their investment research and decision-making. The type and extent of engagement activity will vary depending on the materiality of the issue, and the potential to deliver a positive outcome.

We may collaborate with other investors as part of an engagement strategy if it can contribute to achieving our engagement objectives. Our membership of regional and global organizations facilitates this.

We took part in 365 engagements over 12 months to end March 2025. Many of them were initiated following matters identified in our fundamental investment and voting analysis. Please note that this figure is based on individual interactions and there may be multiple interactions with any one company.

Engagement goals can be both outcome-based and means-based. As mentioned, we engage with company boards to support the ongoing objective of higher levels of accountability, transparency, reporting, and also to drive improvement in relevant sustainability metrics.