General Information

Queen's is registered for GST/HST purposes and therefore is required to charge and collect the applicable GST/HST on all taxable supplies of goods and services made available (sold) in Ontario and in Canada. The HST collected is accounted and reported on a monthly basis by Financial Services to the CRA. Taxable supplies are supplies that are made in the course of a commercial activity and include zero-rated supplies. As a general rule, most services supplied by Queen's are exempt and most goods supplied by Queen's are taxable.

HST collected should be recorded to Account 210080 using the same fund and department as the revenue associated with the HST collected.

The Community is encouraged to review, on a regular basis, all activities which generate external revenue and to determine whether these transactions are taxable for HST purposes. Generally speaking, internal transactions between business units are not taxable for HST purposes as they are within the same entity.

If you have any questions, please contact us.

1.1 General Considerations

Queen's University engages in a variety of sales transactions. Some of these sales are to other Queen's departments (internal sales) and some are to outside vendors (external sales).

Tangible personal property (goods) acquired or produced for resale are taxable unless the property was donated to Queen's or used by another person prior to its acquisition by Queen's. Property (i.e. goods, capital property) that was previously used primarily (>50%) in the University's commercial activities is also taxable.

There are rules governing which tax rate applies on sales to other provinces. This section goes through internal versus external sales, sales to other provinces, tax rates of other provinces, accounting for the taxes collected on sales, and whether the supply is a single or incidental supply.

Some of your sales may actually be to other Queen’s departments. For example, the Campus Computer Store sells many products internally. These “sales” are actually internal transfers for which GST/HST does not apply.

Please also note that Queen’s has many affiliated organizations who are considered external customers for tax purposes. These are organizations who have a connection with Queen’s and typically use Queen’s ChartFields, specifically funds starting with “9”. Funds starting with “9” are called agency funds and organizations using these “9” series funds should apply HST. An exception to this is the following agency funds as they are included on the Queen's University HST return:

- 90009 - Alumni Branches and Classes

- 90011 - Retirees Assoc of Queen's

- 93104 - Queen's/KGH Parking Commission

- 93107 - QU/KGH CoGeneration Facility

GST/HST is only applicable to external sales (link to A/R - Invoicing External Sales) - that is, sales to other companies or individuals. Sales to Queen’s employees are still external sales unless the employee is acting as an agent of Queen’s (purchasing for his or her department for example).

Please refer to the Queen’s website for more information on internal and external transactions.

1.1.2 Where Were The Goods/Services Delivered?

(Place of Supply)

Taxable supplies that are made in Canada will be subject to HST, GST, and/or PST. The place of supply rules determine whether a supplier has made a supply of goods or services in a participating province - that is, a province that uses HST. For all other provinces, GST is charged. If a supply of a good or service is made outside Canada, GST and HST are not typically charged.

Generally, the place of supply will depend on where the supplier delivers a good or service, or the location of the purchaser. It is very important to distinguish between a good and a service as there are different rules for goods than services. As well, there are many exceptions to the general place of supply rules - some of which are listed in the below table.

| Goods & Services Exemptions to General Place of Supply Rules These Have Specific Place of Supply Rules* | |

|---|---|

| Personal Services | Repairs, maintenance, cleaning adjustments, alterations, and photographic-related goods |

| Services in relation to tangible personal property | Services of trustee in respect of a trust governed by an RRSP, RRIP, RESP, TFSA, or RDSP |

| Services in relation to real property | Premium rate telephone services |

| Services in relation to a Location-Specific Event | Computer-related services and internet access |

| Customs brokerage services | Air navigation services |

| Sales of specified motor vehicles | Railway rolling stock supplied otherwise than by way of sale |

| Supplies of intangible personal property that relate to real property | Intangible Personal Property that relates to passenger transportation services |

| Supplies of postage and mail delivery | Supplies of telecommunication services |

| Passenger Transportation services | |

*Refer to GST/HST Technical Information Bulletin B-103 for more information.

The appropriate HST/GST rate must be applied to all external sales for any goods that are sold and delivered to any of the HST participating provinces: Nova Scotia, New Brunswick, Newfoundland and Labrador, Ontario and Prince Edward Island.

For example, if Queen's holds courses in Nova Scotia it must charge the 14% HST which applies to Nova Scotia. Please refer to the section below titled Provincial Tax Rates (section 1.3) to determine the appropriate HST/GST rate.

Goods that are sold and delivered to the non-HST provinces should only be charged the GST (5%).

Due to the complexity of this topic, the CRA has prepared guides with many specific examples:

General guide.

Technical bulletin.

Tax Rates for Provinces (updated as of April 1, 2025):

| Province | Type | HST (%) | GST (%) | PST (%) | Total Tax Rate (%) |

|---|---|---|---|---|---|

| Ontario | HST | 13 | n/a | n/a | 13 |

| New Brunswick | HST | 15 | n/a | n/a | 15 |

| Newfoundland and Labrador | HST | 15 | n/a | n/a | 15 |

| Nova Scotia | HST | 14 | n/a | n/a | 14 |

| Prince Edward Island | HST | 15 | n/a | n/a | 15 |

| British Columbia | GST + PST | n/a | 5 | 7 | 12 |

| Manitoba | GST + PST | n/a | 5 | 7 | 12 |

| Saskatchewan | GST + PST | n/a | 5 | 6 | 11 |

| Quebec | GST + QST* | n/a | 5 | *9.975 | 14.975 |

| Alberta | GST | n/a | 5 | n/a | 5 |

| Northwest Territories | GST | n/a | 5 | n/a | 5 |

| Nunavut | GST | n/a | 5 | n/a | 5 |

| Yukon | GST | n/a | 5 | n/a | 5 |

Printable Provincial Tax Rate Chart (PDF, 120 KB)

Tax collected from a sale is not revenue for Queen's. Any tax collected should be recorded to the appropriate tax account and the same fund and department as the revenue associated with the tax collected (see listing of accounts below). If Queen's is acting as an agent, please refer to the section titled: Taxes Collected on Sales where Queen's has an Agency Agreement (section 1.1.5).

As part of regulatory requirements, once a month Queen's zeros out these tax accounts and remits this tax to the government (CRA) by filing GST/HST returns.

In order to fulfill its tax obligations and file the GST/HST returns correctly, Queen's uses a number of accounts to keep track of GST/HST. The following is a list of commonly used accounts for sales:

| Account | Account Name | Description |

|---|---|---|

| 210024 | AP-GST | GST collected on invoices |

| 210080 | AP-HST Payable Collected | HST collected on sales, HST self-assessed on purchases (including foreign sales) |

| 210087 | PST-Quebec | PST self-assessed, collected and to be remitted to that Province. |

| 210088 | PST-Saskatchewan | PST self-assessed, collected and to be remitted to that Province. |

Please note, if you are thinking of recording tax to a non-participating province (i.e. Saskatchewan or Quebec), please contact HST Help to ensure that the related good/service is taxable and that Queen’s is registered to collect and remit tax with that province. Non-participating provinces have different tax treatments and exemptions than Ontario and the participating provinces.

Please note: this section is not referring to Queen’s agency funds. Funds starting with “9”, which Queen’s has defined as agency funds, are considered external customers and therefore should be charged HST. The Agency referred to in this section, is defined by CRA as outlined below.

When Queen’s, or a department of Queen’s, acts as an agent and the presenter is registered for HST, the presenter must charge and remit the HST on the sale of the tickets sold through Queen’s as the agent. Therefore, the HST collected on the sale of tickets for a presenter registered for HST should be remitted to the presenter for remittance to CRA.

When Queen’s, or a department of Queen’s, acts as an agent and the presenter is not registered for HST, Queen’s must charge and remit the HST on the sales of tickets sold through Queen’s as the agent. Therefore, the HST collected on the sale of tickets for a presenter who is not registered for HST must be remitted to CRA by Queen’s.

Queen’s is acting as an agent in making a transaction on behalf of another person for HST purposes when the following exist:

- Consent on both parties - The principal will generally authorize the agent to do something on the principal’s behalf

- Authority of the agent to affect the principal’s legal position; and, the principal authorizes the agent to enter into contracts with third parties on the principal’s behalf

- The principal’s control of the agent’s actions - The principal maintains some control over the actions of the agent

- Assumption of risk - The agent does not assume the risk of loss from the transaction(s) with a third party

- Accounting practices - The agent will generally record separately revenues received and expenses for costs of goods acquired in its capacity as an agent

- Payment - The agent will generally receive a payment for their services in the form of a set fee

These concepts may be helpful in determining the tax status of a particular sale.

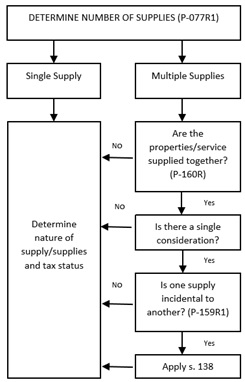

A single supply will have a single tax status (in other words tax will be charged consistently on the whole supply). If a supply is incidental to another, the incidental supply will take on the tax status of the main supply.

First one must determine whether the supply is a single supply. The CRA identifies several criteria that suggest a single supply:

- the property/service is provided by one supplier and to one recipient

- the supplier is not supplying different distinct elements

- the recipient is unaware of specific elements of the supply

- the recipient cannot acquire the elements separately

According to the CRA:

"[T]wo or more elements are part of a single supply when the elements are integral components; the elements are inextricably bound up with each other; the elements are so intertwined and interdependent that they must be supplied together; or one element of the transaction is so dominated by another element that the first element has lost any identity for fiscal purposes."

If a supply is not a single supply, one of the supplies may still be incidental to another. In order to be incidental, the supply must be made with the main supply for a single charge and it must play a minor or subordinate role in relation to the main supply.

The CRA has a policy statement on this topic that contains several examples.

If you have any questions or concerns, please contact us

The CRA's flowchart for this topic (reproduced below) is particularly helpful. S. 138 at the bottom right of the chart refers to incidental supplies.

1.2 Exemptions and Rebates

There are transactions where the GST/HST is not applicable in part or in full. For example, University general exemptions, exempt supplies, zero-rated supplies, direct cost exemptions, sale of goods or services to Provincial Governments, and point of sale rebates including the Ontario First Nations Point of Sale rebate.

In general, most exemptions apply to services while most zero-rated and point of sale rebates apply to goods. There are specific rules for Universities.

Most services provided by a University are exempt, while most goods are taxable. The University cannot choose to ignore an exemption. If the supply is exempt, tax cannot be charged.

The Excise Tax Act contains a general exemption for all services provided by a University. Services are exempt unless they are otherwise made taxable. The following remains taxable despite the general exemption. The Excise Tax Act lists more exceptions than this, but many do not apply to Queen's:

| Exceptions to the University's General Exemption (Need to Charge Tax) |

|---|

| Zero rated goods and services (because tax is 0% - still don't need to charge) |

| Property or services made under a contract for catering for an event or occasion sponsored or arranged by another person who contracts with the institution for catering |

| Most memberships that include a right to participate in recreational or athletic activities or to gain admission to a place of amusement |

| Services of performing artists to a person who makes taxable supplies of admissions |

| Service or membership related to athletic or recreational activities (however some camps are exempt - no tax charged) |

| Right to play in a game of chance |

| Service of instructing individuals in courses (however some are exempt). Please see Example (c) under the Specific Case Examples section below [section 1.3.2 (c)] |

| Admissions to a place of amusement, conference, seminar (or similar event), or a fund raising event. There are specific exemptions for some fund raising events. |

| Cosmetic services. |

The Excise Tax Act then lists further specific exemptions for goods and for certain services provided by Universities. These exemptions override the "exceptions to the rule" listed above. In other words, these remain exempt. Most of them have been addressed above, but here are some others that you may encounter (don't need to charge tax):

- Supplies for a charge that does not exceed direct cost (see the section on Direct Cost Exemption below - section 1.2.4)

- Amateur performances and events

- Long term leases (rentals) of real property (see the section on Rent and Leases below - section 1.3.2 (e))

- Meal plans

1The general exemption also lists "personal property" i.e. goods, but it is extremely rare for it to actually apply.

Zero-rated supplies are goods and services which are taxable at 0% (zero-rated). This means that GST/HST is not charged on the supply of these goods. However, Queen's can claim an input tax credit for the GST/HST paid or payable on expenses made to provide zero-rated sales or supplies. Exports (shipping outside of Canada) is an example of a zero-rated supply that would apply to Queen's.

| List of Zero-Rated Supplies - GST/HST taxable at 0% |

|---|

| Basic groceries - milk, bread, and vegetables |

| Agricultural products - grain, raw wool, and dried tobacco leaves |

| Most farm livestock |

| Most fishery products - fish for human consumption |

| Prescription drugs and drug-dispensing fees |

| Medical devices - hearing aids, artificial teeth |

| Exports |

| Many transportation services - origin or destination is outside Canada |

Goods and services which are exempt from the GST/HST means that you do NOT charge the GST/HST on the supply of these goods and services and you do NOT claim the input tax credits.

Below is a listing of a few exempt supplies that pertain to Queen's.

| Exempt Supplies - no GST/HST |

|---|

| Courses that lead to a certificate or diploma to practice a trade or vocation |

| Tutoring for an individual who takes a course approved for credit |

| Music lessons |

| Child care services (day care - less than 24 hrs a day) for children 14 years old and younger |

| Legal Aid services |

| Most health, medical, and dental services performed by licensed physicians or dentists for medical reasons |

| Long-term residential accommodation (of one month or more), condo fees |

If the University supplies a good for less than its direct cost (not including overhead or staff salaries), the supply is exempt. If the good is sold at direct cost, the University can choose whether to charge that tax.

This exemption may provide a very good opportunity to choose how taxes apply to your sales. For example, your department might want to use this exemption to reduce the amounts charged to students. On the other hand, commercial businesses are often unaffected by taxes (if a business’ sales are taxable, it can fully recover the taxes it pays), so you might choose to charge tax in order to recover more of your own costs through input tax credits. Please see the section on Input Tax Credits [section 2.2.6].

The direct cost exemption can also apply to services; most often when Queen’s purchases a service for direct resupply. However, many services provide by Queen’s are exempt even without the direct cost exemption.

Example

The University purchases calculators from a retailer for the purpose of reselling them to students. The retailer charges Queen’s $10 + $1.30 HST for each calculator. In this example, Queen’s has two choices if it wants to recover its costs:

Option 1 - Direct Cost Exemption:

$10 + $1.30 HST = $11.30

$1.30 HST x 73.77% rebate on the HST = $0.96 rebate

Direct Cost to Queen’s = $11.30 - $0.96 = $10.34

Therefore, Queen’s can charge $10.34 and no HST to students.

Queen’s is not making a profit in this situation, they are only recovering their costs

Option 2 - Commercial Sale:

$10 + $1.30 HST = $11.30

Direct Cost to Queen’s = $10.00

Therefore, Queen’s can charge $10 (or more) plus 13% HST to students.

Queen’s can fully recover the $1.30 it paid to the retailer as an input tax credit (ITC) because it is a commercial resale.

If Queen’s wants to make a profit, the supply will be taxable.

The governments of New Brunswick, Newfoundland and Labrador, Nova Scotia, Ontario, and Prince Edward Island provide a point-of-sale rebate on the provincial part of the HST payable on qualifying items. When a point-of-sale rebate is provided, Queen's would only charge and collect the 5% federal part of the HST payable on the sale of these items.

Qualifying Items for the Point-Of-Sale Rebate and in which Province it Applies:

| Province | Books | Children's Items | Feminine Hygiene Products | Qualifying Heating Oil | Newspaper | Qualifying Food & Beverage |

|---|---|---|---|---|---|---|

| New Brunswick | Yes | No | No | No | No | No |

| Newfoundland and Labrador | Yes | No | No | No | No | No |

| Nova Scotia | Yes | Yes | Yes | No | No | No |

| Ontario | Yes | Yes | Yes | No | Yes | Yes |

| Prince Edward Island (PEI) | Yes | Yes1 | No | Yes | No | No |

Note 1 - For PEI, Children's items do not include children's diapers.

Effective September 1st, 2010 there is a point of sale rebate on the 8% Provincial component of HST for people that qualify as Status Indians. This means that only the 5% federal portion of HST would be charged and collected on the supply of certain goods or services to people who qualify as Status Indians.

Ontario Status Indians will be required to present a valid Certificate of Indian Status identity card issued by Indian and Northern Affairs Canada to the vendor at the time of purchase.

Only certain property and services apply to this exemption. Please review the First Nations Guide for more detailed information.

If certification is provided, no GST/HST is to be charged on the sale of goods or services to the Provincial Governments and their recognized bodies for:

- Quebec

- Manitoba

- Saskatchewan

- Alberta

- Yukon and Northwest Territories

However, Federal, Municipal and Provincial Governments (not listed above) do pay GST/HST. As well, sales to the Ontario government and its agencies are taxable for HST purposes.

If you have any questions or concerns, please contact us.

1.3 HST Rates by Sales Type

The Quick Reference Guide - HST Rates by Sales Type chart has been developed to assist departments to determine if a sale should contain HST. In addition to the Quick Reference Guide, specific examples of situations you may encounter at Queen's are given below.

This table lists both taxable and exempt supplies of goods and services for both HST and GST purposes. If the sale is taxable, then one must consider the overriding exemption provisions to determine if the revenue source remains taxable.

Quick Reference Guide - HST Rates by Sales Type (PDF, 173 KB)

If you have any questions or concerns, please contact us.

Qualifying books are eligible for a point of sale rebate on the provincial portion of the HST. This means that you should only charge 5% tax on books.

| Qualifying Books are Defined to be: |

|---|

| A printed book or an update of a printed book |

| An audio recording 90% or more of which is a spoken reading of a printed book |

| A bound or unbound printed version of scripture of any religion |

| A printed book with a read-only medium that is wrapped, packaged or prepared for sale as a single product where the read-only medium contain 90% or more of the value of which is reasonably attributable to a reproduction of a printed book and/or material that makes specific reference to the printed book and its content, and that supplements and it's integrated with that content |

| A printed book with a read-only medium or a right to access a website (or both) that is wrapped, packaged or prepared for sale as a single product specially designed for use by students enrolled in a qualifying course where the read-only medium or website contains material related to the subject matter of the printed book.1 |

Items that do not count as a qualifying book (such as e-books) are most often taxable at 13% (Ontario HST).

As a result, "books" that are in electronic format, e.g., a CD, will not be considered as a qualifying book for GST/HST rebate purposes and will be not be eligible for the available rebates. Please note that the rebates for books apply to ALL books, and not just those purchased by the library.

As of 2018, the Federal Book rebate is no longer available on books for resupply. This includes:

• Books for resale – example: books sold at the bookstore

• Books for transfer – example: books provided to students as part of course fee

More information on what qualifies as a book for purposes of the rebates can be found on the CRA website.

In order to determine whether a conference, seminar, or event is taxable, it is important to consider what the recipient actually receives. Attendees typically pay for the right to attend the conference, seminar, or event, but they may instead be paying for a particular service or good and the conference is secondary.

The Excise Tax Act does not define the terms conference, seminar, or event, so the usual dictionary definitions should be used.

Assuming that the payee is paying for a right to attend, the following rules apply:

- Admission to a conference, seminar, or similar event is taxable.

- Admission to a place of amusement is also a taxable supply.

- Admission to an amateur performance or athletic event is exempt as long as the performers or athletes are not paid.

- Supplies that are made at an event or conference are often taxable. For example, clothing sold at an amateur athletic event is taxable even though admission to the event is exempt.

Making a conference or event taxable may actually be beneficial for the University. Queen's will be able to recover ITCs rather than partial rebates. Conference attendees will pay more, but they may be able to recover ITCs themselves if they are representing a commercial business.

A Few Examples

Example 1 : Queen's is organizing a conference for physics researchers in Ontario and charges admission for that conference. Queen's also plans to sell books to conference attendees who wish to purchase them. The admission is taxable at 13%, and the books are taxable at 5% as qualifying books (unless the Direct Cost Exemption applies). Queen's can claim full ITCs on its expenses to host the conference and to supply the books.

Example 2 : Queen's music puts on a public performance on campus and charges admission. The musicians are all unpaid students at Queen's. The admission is GST/HST exempt. Queen's could claim its normal rebates on expenses incurred to put on the performance. If, on the other hand, the performers were paid, the admission would be taxable at 13%. If the student musicians are unpaid, but Queen's advertises in the Queen's Gazette that a paid professional musician who they have invited will also be playing, the event is taxable at 13%. In the two taxable scenarios, Queen's can claim full ITCs on its expenses to put on the performance (which would include the tax that the professional musician charges to Queen's).

Many of the course fees that Queen's charges to students are exempt. (As per Schedule V, Part III of the Excise Tax Act.)

- As a general rule, tuition is exempt if the course gives credit towards a diploma or degree. Fees for services and memberships that must be paid by students in these courses (mandatory fees) are also exempt. Most of the courses that Queen's offers are covered by this exemption.

- Courses leading to certificates, diplomas, licenses, or similar documents that allow a person to practise a trade or vocation are also exempt.

- English and French courses that form part of a program of second-language instruction are exempt.

Non-degree courses are often taxable, but if they are part of a larger program of two or more courses, they may be exempt. If you offer non-degree courses, you are encouraged to contact financial services for more information. Examples of taxable programs on campus include the Queen's School of Business Executive Education courses.

A pure service provided by Queen's is exempt due to the Educational Services Exemption in the Excise Tax Act. Please see the section on Queen's General Exemption (Educational Services Exemption). However, it is important to look at what is actually being provided to the purchaser. Sometimes these "services" are not truly services. For example, the purchaser may instead be paying for a good. Goods sold by the University are typically taxable.

For example, if a company contracted the Chemistry department to run a sample for them, using Queen's NMR machines and provide the results, the supply would be exempt. Fundamentally, Queen's would be supplying a service.

If instead, a company were to contact Queen's to prepare a sample for them and mail it to them, the supply would be taxable. Fundamentally, Queen's would be supplying a good and not the service of preparing the good.

Leases by the University (such as a rental of a building or room) are exempt as long as they are for periods of one month or longer. Short term rentals and leases remain taxable.

The University may elect to make long term leases taxable on a property by property basis. If the University makes such an election, the lease must be treated as taxable until the election is revoked.

Real property also has its own set of rules. For example, residential rent (for example, of a house or apartment to an individual) is exempt regardless of who supplies it.

If you have any questions or concerns regarding this topic, please contact: hst.help@queensu.ca

Most research grants are exempt because the funds are not consideration for a supply. In other words, the granting agency does not receive anything in return (except perhaps something nominal like a progress report).

For research grants that are provided by for-profit agencies ("contract research"), it is important to keep in mind that the grant may in fact be consideration for a supply. If that supply is taxable, the "grant" may be taxable, and Queen's should collect and remit tax on the payment. Luckily, most commercial entities can recover 100% ITCs on their expenses; in other words, they can fully recover the tax that is charged to them.

A Few Examples

Example 1 : Natural Sciences and Engineering Research Council of Canada (NSERC) provides a researcher at Queen's with a grant to perform research in the area of physics. The fact that the grantor is a government non-profit agency is a good indication that the grant has a public purpose (most likely to improve Canadian research in a particular field). The researcher is required to report back to NSERC, but the main purpose of this is accountability. The grant is exempt.

Example 2 : Bombardier provides a grant to Queen's Engineering. In return for the funds, Bombardier expects Queen's to provide them with a working prototype based on their specifications. In this case, the "grant" is consideration for a taxable supply that Queen's is providing to Bombardier. The fact that Bombardier is a commercial entity is further evidence of the fact that the payment is not a true grant, but it is not the determining factor.

This can be a complex topic, and it might be helpful to review the CRA's guide on transfer payments.

The following flow chart from that guide is also particularly helpful: